Fact-checked by the Prime Rate editorial team

Quick Answer

To get the best deal on a car loan, you need to understand how the prime rate directly shapes the interest rate a lender offers you. The federal funds rate target range sits at 4.25%–4.50%, keeping the prime rate at 7.50%, which means auto loan rates for well-qualified buyers typically start around 6%–8% and climb significantly for lower credit scores. Shop at least three lenders, check your credit score, and get pre-approved before stepping into a dealership.

Understanding prime rate car loans is one of the most practical financial skills you can develop before financing a vehicle. The U.S. prime rate stands at 7.50%, set by major commercial banks in direct response to the Federal Reserve’s federal funds rate, and that single number ripples outward to affect the rate on virtually every auto loan in the country. According to Federal Reserve H.15 selected interest rate data, the prime rate has held steady since December 2024, giving buyers a relatively predictable borrowing environment.

Why does this matter? Auto loan rates remain historically elevated compared to the near-zero rate environment buyers enjoyed between 2020 and 2022. The average new car loan rate for a 60-month term was hovering around 8.01% in early 2025, according to Bankrate’s auto loan rate tracker. Buyers who don’t understand how the prime rate connects to their loan offer risk paying thousands of dollars more than necessary over the life of a loan.

This guide is for anyone financing a car in 2025, whether it’s your first auto loan or your fifth. By the time you finish, you’ll know exactly how the prime rate determines your rate, what lenders look for, and how to negotiate a deal that works in your favor regardless of where rates are headed.

Key Takeaways

- The U.S. prime rate is 7.50%, directly influencing every auto loan rate offered by banks, credit unions, and captive lenders, according to the Federal Reserve.

- The average new car auto loan rate for a 60-month term is approximately 8.01% in early 2025, meaning most borrowers pay a spread of roughly 0.5%–2% above the prime rate, per Bankrate.

- Borrowers with a credit score below 600 can face auto loan rates exceeding 15%–20%, costing thousands more over a 60-month term compared to prime borrowers, according to Experian’s State of the Automotive Finance Market.

- Getting pre-approved from at least 3 lenders before visiting a dealership can save the average buyer $1,000 or more in total interest, based on research from the Consumer Financial Protection Bureau (CFPB).

- Credit unions typically offer auto loan rates 1%–2% lower than traditional banks for the same borrower profile, according to National Credit Union Administration (NCUA) data.

- Every 1% increase in your auto loan APR on a $30,000, 60-month loan adds approximately $780 in total interest over the life of the loan, making rate comparison one of the highest-return steps in the car-buying process.

In This Guide

- How does the prime rate affect car loan interest rates?

- What is a good auto loan rate right now and how do I know if I’m getting one?

- How does my credit score affect the auto loan rate I get?

- How do I get pre-approved for a car loan before going to the dealership?

- Should I use dealer financing or get my own loan from a bank or credit union?

- How do I negotiate my auto loan rate to get the best deal?

- Frequently Asked Questions

Step 1: How Does the Prime Rate Affect Car Loan Interest Rates?

The prime rate acts as a baseline that lenders add a margin on top of to set your actual auto loan APR. When the Federal Reserve raises the federal funds rate, commercial banks raise the prime rate in lockstep, and loan rates across the board follow within days.

How This Works in Practice

The prime rate is set at 3 percentage points above the federal funds rate target. With the Fed’s rate at 4.25%–4.50%, the prime rate lands at 7.50%, as tracked by the Federal Reserve’s H.15 release. Lenders then add a “spread” based on your creditworthiness, loan term, and whether you’re buying new or used. A buyer with excellent credit might get prime rate plus 0.5%, while a subprime borrower could face prime rate plus 8% or more.

Auto loans are not always directly indexed to the prime rate the way a home equity line of credit is. But the prime rate signals the overall cost of money. When it rises, lenders’ funding costs increase, and those costs get passed to borrowers through higher APRs.

What to Watch Out For

Dealer financing desks often do not voluntarily explain the connection between the prime rate and your loan offer. They quote a monthly payment, not an APR, which makes it easy to obscure how much a rate increase costs you. Always ask for the full APR and the total interest paid over the life of the loan before agreeing to anything.

The prime rate has changed 11 times since March 2022, rising from 3.25% to a peak of 8.50% before the Fed began cutting in late 2024. Each of those moves directly shifted auto loan rate benchmarks used by banks and credit unions nationwide.

To understand the broader relationship between benchmark rates and your borrowing costs, see our explainer on how the prime rate affects personal loan rates. The same mechanics apply to auto lending.

Step 2: What Is a Good Auto Loan Rate Right Now and How Do I Know If I’m Getting One?

A good auto loan rate is one that falls at or below the current average for your credit tier. Right now, that average for a 60-month new car loan is approximately 8.01% APR for the overall market, with well-qualified borrowers getting rates starting closer to 5.5%–7%.

How to Benchmark Your Rate Offer

Use published rate data from Bankrate’s auto loan rate tracker and the Federal Reserve’s G.19 Consumer Credit report to compare what lenders are actually charging. The Fed’s G.19 release breaks out average commercial bank auto loan rates by loan term, making it one of the most reliable benchmarks available. For used vehicles, rates typically run 1.5%–3% higher than new car rates for the same borrower.

The table below shows a realistic snapshot of auto loan rate ranges by credit tier and loan type in early 2025.

| Credit Score Range | Credit Tier | Avg. New Car APR (60-mo) | Avg. Used Car APR (60-mo) | Monthly Payment on $30K |

|---|---|---|---|---|

| 781–850 | Super Prime | 5.64% | 7.02% | $574 |

| 661–780 | Prime | 7.01% | 9.52% | $594 |

| 601–660 | Near Prime | 9.82% | 13.52% | $636 |

| 501–600 | Subprime | 13.74% | 18.91% | $692 |

| 300–500 | Deep Subprime | 15.77% | 21.18% | $724 |

Source: Experian State of the Automotive Finance Market, Q1 2025. Monthly payment calculations assume a 60-month loan term with no down payment for illustration purposes.

What to Watch Out For

Dealers sometimes quote a rate that is higher than what the lender actually approved, pocketing the difference as profit. This practice is known as “dealer markup” or “dealer reserve,” and the Consumer Financial Protection Bureau (CFPB) has flagged it as a potential source of discriminatory pricing. Always get the buy rate (the lender’s actual approved rate) in writing if possible.

The difference between a 5.64% APR (super prime) and a 15.77% APR (deep subprime) on a $30,000, 60-month loan is approximately $6,600 in additional interest, nearly the cost of a year’s worth of car insurance for most drivers.

Step 3: How Does My Credit Score Affect the Auto Loan Rate I Get?

Your credit score is the single biggest factor lenders use to determine your auto loan rate, more than your income, the car’s price, or the loan term. A score above 780 typically earns the best available rates, while anything below 600 places you in subprime territory with sharply higher APRs.

How to Check and Strengthen Your Credit Before Applying

Pull your credit reports for free at AnnualCreditReport.com, the only federally authorized source for free reports from all three bureaus: Equifax, Experian, and TransUnion. Look specifically for errors, old derogatory marks, or high credit utilization. These are the fastest levers to fix. Paying down a credit card balance to below 30% utilization can lift a score meaningfully within one to two billing cycles.

For a detailed, step-by-step approach to raising your score before a major loan application, our guide on how to build credit from scratch covers the foundational strategies, including secured cards, credit builder loans, and authorized user status. Many of the same tactics apply if you’re rebuilding after a rough patch.

What to Watch Out For

Multiple auto loan applications in a short window will generate multiple hard inquiries on your credit report. The major credit scoring models, including FICO Score 8 and VantageScore 4.0, treat all auto loan inquiries made within a 14- to 45-day window as a single inquiry for rate-shopping purposes. Do not let fear of hard pulls stop you from comparing at least three to five lenders.

If your credit score is sitting just below a tier threshold, for example, at 658 instead of 661, it may be worth waiting 30 to 60 days to pay down balances and boost your score into the prime tier. Moving from near-prime to prime can reduce your APR by 2%–3%, saving hundreds of dollars per year on a typical loan.

The gap between credit tiers is not marginal, it is dramatic. According to Experian’s State of the Automotive Finance Market, a borrower who spends three months improving their credit before applying for a car loan could save more in interest than most people earn in a year of contributions to a high-yield savings account. The math consistently favors patience over urgency.

Step 4: How Do I Get Pre-Approved for a Car Loan Before Going to the Dealership?

Getting pre-approved for an auto loan before visiting a dealership gives you a firm rate offer in hand, which transforms the negotiation dynamic entirely. You’re shopping with cash equivalents rather than asking for permission. The process takes 15–30 minutes per lender and can realistically be completed in a single afternoon.

How to Get Pre-Approved: Step by Step

Start with your existing bank or credit union, where you already have a relationship. Then apply at one or two additional institutions: a national bank like Bank of America or Chase, plus a credit union you can join (many have open membership requirements). Online lenders such as LightStream (a division of Truist Bank) and Capital One Auto Finance offer fast pre-approvals without visiting a branch.

When you apply, you will typically need to provide:

- Government-issued photo ID

- Social Security number

- Proof of income (recent pay stubs or tax returns for self-employed borrowers)

- Proof of residence (utility bill or bank statement)

- Estimated vehicle price and whether it is new or used

Pre-approval letters are typically valid for 30 to 60 days, giving you a comfortable window to shop. Understanding how your overall budget fits a car payment is easier with a solid monthly budget framework. Our guide on how to create a monthly budget that actually works can help you determine what payment you can realistically afford before you even walk into a showroom.

What to Watch Out For

A pre-approval is not a guarantee of final approval. Lenders will do a final verification once you submit the actual vehicle details, and the rate could change if the vehicle does not meet their requirements (such as a used car that is too old or has too many miles). Ask each lender about their vehicle age and mileage restrictions upfront.

Do not let a dealership’s finance manager run your credit before you have shared your pre-approval offer. Some dealers run your application with multiple lenders simultaneously without disclosing it, which can generate unnecessary hard inquiries and give them leverage over which lender gets the deal, and how much markup they earn.

Step 5: Should I Use Dealer Financing or Get My Own Loan from a Bank or Credit Union?

In most cases, getting your own financing from a bank or credit union before visiting the dealership gives you more control and a lower rate. That said, dealer financing can occasionally win, especially when manufacturers offer promotional rates like 0% APR on new vehicles.

How to Evaluate Both Options

Dealer financing works through the dealer’s finance and insurance (F&I) department, which submits your application to a network of lenders, including captive finance arms like Toyota Financial Services, Ford Motor Credit, and GM Financial. These captive lenders sometimes offer below-market promotional rates, but only on specific models and only to well-qualified buyers. If you don’t qualify for the promotional rate, the dealer will present a standard market rate that often includes a markup.

Credit unions consistently offer some of the lowest auto loan rates available to the general public. According to NCUA data, the average credit union new auto loan rate is typically 1%–2% below comparable commercial bank rates for the same credit tier. If you are not already a credit union member, many allow you to join by making a small donation to a partner nonprofit.

This is also worth considering in the context of how the prime rate affects all forms of borrowing. Our related article on how the prime rate affects your mortgage and home equity loan illustrates the same lender-shopping principle across different loan types.

What to Watch Out For

The dealer’s F&I office is a profit center. Products like extended warranties, gap insurance, credit life insurance, and paint protection packages are routinely rolled into the loan amount, increasing both your principal and the total interest you pay. Each add-on financed at 8% APR over 60 months costs significantly more than its sticker price.

If a dealer offers you a promotional rate like 1.9% APR or 0% APR, compare it against the alternative: sometimes manufacturers offer a cash rebate instead of the low rate. On a $35,000 vehicle, a $3,000 rebate financed at 6.5% through your own lender can cost less in total than the promotional rate with no rebate. Run the math on both scenarios before deciding.

Step 6: How Do I Negotiate My Auto Loan Rate to Get the Best Deal?

Negotiating your auto loan rate is straightforward when you arrive with a pre-approval in hand and knowledge of the current prime rate environment. Your pre-approval becomes a floor. Ask the dealer to beat it, and you may get a lower rate with no additional effort.

How to Negotiate Effectively

Present your pre-approval letter to the F&I manager and say clearly: “I have financing arranged at [X]%. Can you beat that?” Dealers earn a referral fee for every loan they send to a lender, which gives them motivation to match or undercut your rate in many cases. If they can beat your pre-approval rate by at least 0.25%, it may be worth accepting their financing, but read every document carefully before signing.

Negotiate the vehicle price and the financing separately. A classic dealer tactic is to agree to a lower purchase price only if you use their financing, or vice versa. Keep the two conversations distinct, and confirm each agreed number in writing before moving to the next item.

Understanding how debt and interest interact across your finances can also help you make smarter decisions here. If you already carry high-interest debt, our guide on how to pay off debt fast using the snowball vs. avalanche method may help you prioritize which balances to attack first, including whether taking on a car loan right now is the optimal move for your financial picture.

What to Watch Out For

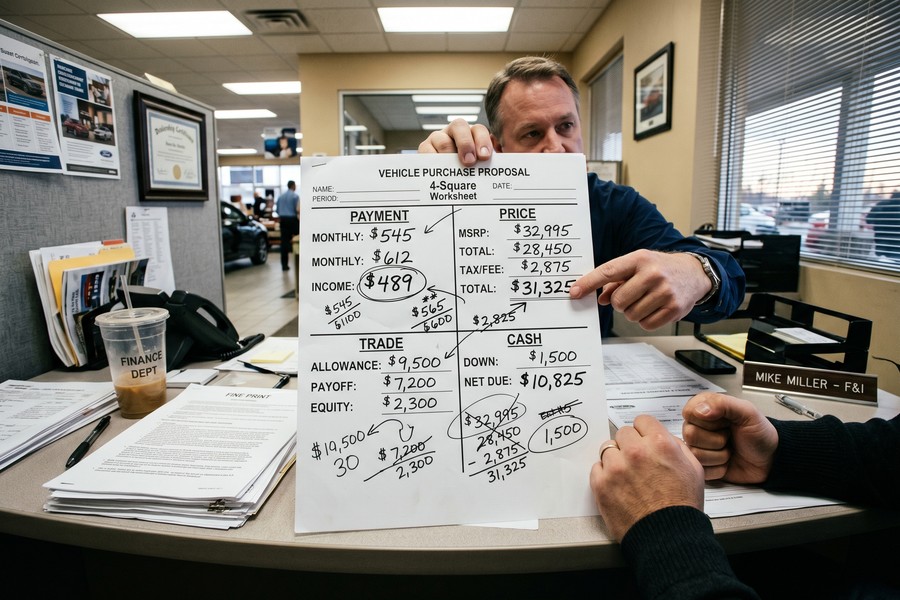

Watch for four-square worksheets that blend purchase price, trade-in value, down payment, and monthly payment into a single confusing grid. This format is specifically designed to make it hard to evaluate any one number in isolation. Ask for each component to be broken out on separate lines, and do not agree to a monthly payment without knowing the APR and total loan cost.

Consumers who walk into a dealership with a pre-approval and knowledge of current market rates are in a fundamentally different negotiating position than those who rely entirely on the dealer’s financing options. The preparation alone, according to the CFPB, can be worth hundreds to thousands of dollars in total savings.

Be cautious about extending your loan term to lower the monthly payment. A 72- or 84-month loan lowers your monthly outlay but dramatically increases total interest paid and creates a higher risk of being upside-down on the loan, meaning you owe more than the vehicle is worth. The CFPB recommends keeping auto loan terms to 60 months or fewer whenever possible.

Also keep in mind that the prime rate can change at any Federal Reserve meeting. If the Fed signals future cuts (something worth monitoring through our coverage of what happens to your savings when the prime rate rises), waiting a few months before signing could yield a lower rate. But timing the market is risky, and a bird in hand, today’s approved rate, is usually worth more than speculation.

Frequently Asked Questions

How much does the prime rate directly change my car loan APR?

The prime rate does not directly set your car loan APR, but it serves as the primary benchmark lenders use to price auto loans. When the prime rate rises by 0.25%, auto loan rates typically rise by a similar amount within weeks, because banks’ cost of funding increases. Your actual APR reflects the prime rate plus a margin based on your credit score, loan term, and vehicle type, as explained by the Federal Reserve’s G.19 consumer credit data.

Is it better to get a shorter or longer loan term when the prime rate is high?

When the prime rate is high, a shorter loan term is almost always the better financial choice. Shorter terms carry lower interest rates, typically 0.25%–0.75% less than 72- or 84-month loans, and you pay off the balance before interest accumulates significantly. The tradeoff is a higher monthly payment, so use a loan calculator to confirm the payment fits your budget before committing. The CFPB’s auto loan tool lets you compare term scenarios side by side.

Can I refinance my car loan if the prime rate drops?

Yes. Refinancing a car loan when rates fall is one of the most underutilized money-saving moves in personal finance. If the prime rate drops by 1% or more after you take out your loan, or if your credit score improves significantly, refinancing could reduce your APR and save hundreds in interest. Contact your bank, credit union, or an online lender like LightStream or Consumers Credit Union to check your new rate before your next payment is due.

What credit score do I need to get a prime rate on a car loan?

To receive a rate close to the prime rate, or even below it through promotional financing, you generally need a credit score of 720 or higher, placing you in the prime or super-prime tier. Borrowers with scores in the 661–720 range typically receive rates 1%–3% above the best available offers. For guidance on reaching those thresholds, our detailed overview of what is a good credit score and what you can do with it breaks down each range and the benefits that open up at each level.

Should I put more money down to offset a high interest rate environment?

Yes. A larger down payment reduces your principal, which directly reduces the total interest you pay regardless of the APR. Putting down 20% or more also helps you avoid being underwater on the loan, since new vehicles depreciate roughly 15%–25% in the first year, according to Carfax depreciation data. If you cannot afford 20% down, gap insurance becomes more important. Either way, minimizing the financed amount is the right instinct.

Does getting pre-approved hurt my credit score?

Pre-approval applications generate a hard inquiry, which can temporarily reduce your credit score by 2–5 points per inquiry. However, all auto loan inquiries made within a 14- to 45-day window are counted as a single inquiry under FICO’s rate-shopping rules, so applying to multiple lenders in a concentrated timeframe has minimal impact. The small, temporary score dip is almost always worth the savings from finding a lower rate.

Are credit unions really better than banks for auto loans?

For most borrowers, yes. Credit unions offer auto loan rates that are 1%–2% lower on average than commercial banks for equivalent credit profiles, according to NCUA data. This is because credit unions are nonprofit, member-owned cooperatives with no shareholders to pay. The main limitation is membership eligibility, but most people qualify for at least one credit union through their employer, a community organization, or a family member.

What happens to my prime rate car loan if the Fed cuts rates after I sign?

If you have a fixed-rate auto loan, which is standard for most car loans, a Fed rate cut does not automatically change your existing APR. Your rate is locked at signing. A rate cut does, however, create a refinancing opportunity: once the prime rate falls and lenders adjust their offers, you can apply to refinance into a lower rate. Monitor the Fed’s FOMC meeting schedule and compare refinance offers if the prime rate drops 0.50% or more from your original loan date.

How do I calculate the total interest I’ll pay on a car loan?

Multiply your monthly payment by the total number of payments, then subtract the original loan principal. A $30,000 loan at 8% APR for 60 months carries a monthly payment of approximately $608, for a total of $36,480 paid, meaning $6,480 in total interest. Use the CFPB’s auto loan calculator to model different rate and term combinations before you commit.

Should I pay cash for a car or finance it when rates are high?

If you have the cash and would not deplete your emergency fund, paying cash can save you thousands in interest in a high-rate environment. However, if the money could earn more in a high-yield savings account or investment than the loan costs you in interest (after taxes), financing may be the more efficient financial move. Run a comparison using the loan’s actual APR versus your money’s guaranteed return rate before deciding.

Sources

- Federal Reserve, H.15 Selected Interest Rates (Prime Rate Data)

- Federal Reserve, G.19 Consumer Credit Release (Auto Loan Rates)

- Experian, State of the Automotive Finance Market, Q1 2025

- Consumer Financial Protection Bureau, Auto Loans Consumer Tool

- National Credit Union Administration, Credit Union Call Report Data

- AnnualCreditReport.com, Free Credit Reports (All Three Bureaus)

- Federal Reserve, FOMC Meeting Schedule and Rate Decisions