Quick Answer

To create a monthly budget that actually works, calculate your net income, list all fixed and variable expenses, assign every dollar a category using a framework like the 50/30/20 rule, and review your spending weekly. As of July 2025, Americans who follow a written budget report saving an average of $200–$300 more per month than those without one.

Knowing how to create a monthly budget is the single most impactful financial skill you can develop. A NerdWallet survey found that only 32% of American households maintain a detailed monthly budget, yet budgeters consistently report lower debt levels and higher emergency savings. The gap between knowing budgeting matters and actually doing it comes down to a clear, repeatable process.

This guide breaks that process into five concrete steps. You will learn which budgeting frameworks work best for different income types, how to handle irregular expenses, and what tools make tracking automatic. Every recommendation here is grounded in data, not generic advice.

Key Takeaways

- The 50/30/20 rule — allocating 50% to needs, 30% to wants, and 20% to savings — is endorsed by the Federal Trade Commission as a reliable starting framework for most households.

- Americans carry an average credit card balance of $6,501, according to Experian’s 2024 State of Credit report — a number a disciplined monthly budget directly reduces over time.

- The Consumer Financial Protection Bureau (CFPB) reports that households with a written budget are 2x more likely to have three months of emergency savings than those without one, per their Financial Well-Being research.

- Budgeting app users save an average of $600 more per year than non-users, according to Forbes Advisor’s 2024 budgeting statistics — making the right tool a measurable advantage.

- The Bureau of Labor Statistics reports that U.S. households spend an average of $6,081 per month on total expenditures, per the 2023 Consumer Expenditure Survey — giving you a real benchmark to compare your own spending.

In This Guide

- Why Do Most Monthly Budgets Fail?

- How Do You Calculate Your True Monthly Income?

- Which Budgeting Framework Should You Use?

- How Do You Track and Categorize Your Spending?

- How Do You Handle Irregular Expenses and Financial Setbacks?

- How Often Should You Review and Adjust Your Budget?

- Frequently Asked Questions

Why Do Most Monthly Budgets Fail?

Most monthly budgets fail because they are built on estimated income and ignored irregular expenses — not because people lack discipline. The structure is wrong before the first dollar is spent.

The three most common failure points are underestimating variable expenses, failing to account for annual bills spread across twelve months, and building a budget too restrictive to maintain. Research from behavioral economics studies cited by Psychology Today shows that overly rigid spending plans trigger the same psychological resistance as crash diets.

The Biggest Overlooked Expense Category

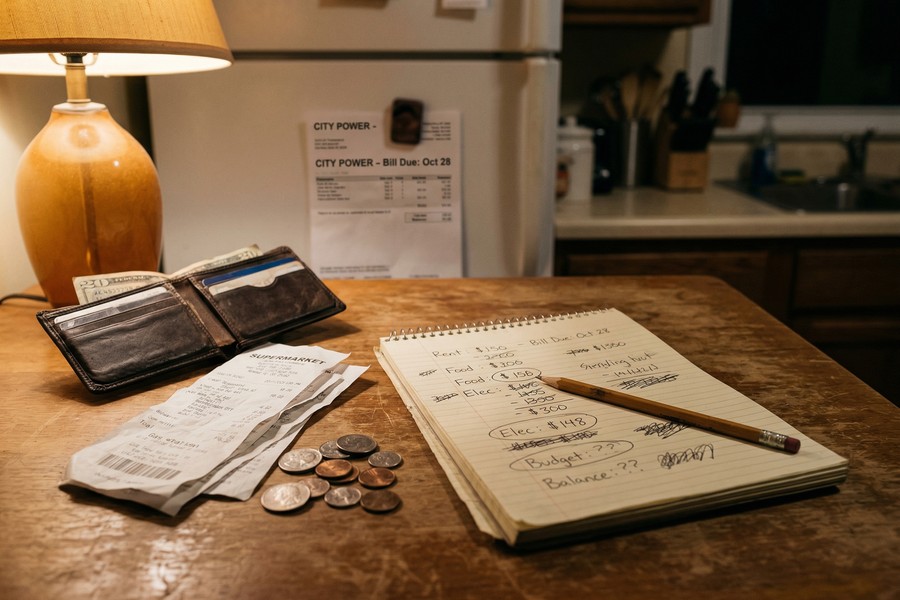

Irregular expenses — car registration, annual insurance premiums, holiday gifts — are the silent budget killers. Most people only budget for monthly recurring bills and are blindsided when a $1,200 car insurance renewal arrives. The fix is dividing every annual or semi-annual expense by 12 and setting that amount aside each month.

According to the Bureau of Labor Statistics Consumer Expenditure Survey, the average American household spends $2,481 per year on entertainment and personal care combined — categories that rarely appear in first-draft budgets.

How Do You Calculate Your True Monthly Income?

Your monthly budget must be built on net income — the amount deposited into your account after taxes, not your gross salary. Using gross income is one of the most common errors new budgeters make.

Add up all consistent income sources: your primary paycheck, side income, freelance payments, and any recurring transfers. If your income varies month to month, use your lowest earning month from the past six months as your baseline. This conservative approach prevents overspending during high-income months and builds a natural buffer.

Handling Variable and Freelance Income

Self-employed individuals and freelancers face a harder calculation. The CFPB recommends setting aside 25–30% of every payment for taxes before budgeting the remainder. After that tax reserve, treat what remains as your spendable income and budget from there. If you carry high-interest debt, consider reviewing debt consolidation loan options as a way to simplify repayment alongside your new budget.

Which Budgeting Framework Should You Use?

The best budgeting framework is the one simple enough to maintain consistently. For most households, the 50/30/20 rule is the ideal starting point — but zero-based budgeting and envelope budgeting each serve specific financial situations better.

Learning how to create a monthly budget means choosing a structure that matches your income pattern, your spending habits, and your financial goals. No framework works if it requires two hours of weekly maintenance you will never do.

Comparing the Top Three Budget Frameworks

| Framework | Best For | Savings Target | Complexity |

|---|---|---|---|

| 50/30/20 Rule | Salaried employees, beginners | 20% of net income | Low |

| Zero-Based Budget | Detail-oriented planners, debt payoff | Every dollar assigned | High |

| Envelope Method | Cash users, overspenders in specific categories | Variable by envelope | Medium |

| Pay-Yourself-First | Savers who struggle with consistency | 10–20% automated | Low |

“A budget is not a restriction — it is a spending permission slip. When you assign every dollar a job before the month begins, you remove the guilt from every purchase inside those boundaries.”

The 50/30/20 Rule in Practice

On a $5,000 net monthly income, the 50/30/20 rule allocates $2,500 to needs (rent, utilities, groceries), $1,500 to wants (dining, subscriptions, entertainment), and $1,000 to savings and debt repayment. If your needs exceed 50% — as they do for many renters in high-cost cities — reduce the wants category first before touching savings.

Automate your 20% savings transfer on the same day your paycheck clears. Treating savings as a fixed, non-negotiable bill — not money left over at the end of the month — is the single habit that separates consistent savers from everyone else. Pair this with a high-yield savings account to earn meaningful interest on the money you set aside.

How Do You Track and Categorize Your Spending?

Effective tracking requires reviewing every transaction at least once per week — not waiting until month-end when it is too late to adjust. Real-time awareness is what separates a budget that works from a budget that exists on paper.

You have three main tracking options: budgeting apps, spreadsheets, or pen and paper. Each works, but the right tool depends on your habits. Apps like YNAB (You Need a Budget) and Monarch Money connect directly to bank accounts and categorize transactions automatically, reducing manual entry to minutes per week.

Setting Up Spending Categories

Start with six core categories: housing, transportation, food, utilities, savings/debt, and discretionary. Break each into subcategories only if a specific area needs tighter control. Over-categorizing at the start creates maintenance fatigue. Watch out for subscription creep — small recurring charges that quietly accumulate across streaming services, apps, and memberships without appearing in any single large transaction.

The average American household spends $219 per month on subscriptions — more than double what most people estimate — according to Forbes Advisor’s 2024 budgeting research. A monthly budget audit often reveals $50–$100 in unused or duplicate services.

How Do You Handle Irregular Expenses and Financial Setbacks?

The most resilient budgets include a dedicated sinking funds category — money saved monthly for predictable but irregular expenses. This one addition prevents most budget failures.

A sinking fund works by dividing a known future expense by the number of months until it is due. A $1,200 annual car insurance bill becomes a $100 monthly line item that never surprises you. Apply this logic to every non-monthly expense: home maintenance, medical co-pays, travel, and holiday spending.

Budgeting Through Financial Setbacks

Job loss, medical bills, and emergency repairs will test any budget. The key is knowing your bare-bones budget in advance — the absolute minimum you need each month for housing, food, utilities, and transportation. When a setback hits, you drop to that floor immediately rather than guessing what to cut. For a deeper strategy on navigating disruptions without abandoning your financial plan, see our guide on handling a financial setback without resetting your entire plan.

If debt repayment is straining your budget, services like the National Foundation for Credit Counseling (NFCC) offer free or low-cost budget counseling. Their advisors can help restructure payment plans without requiring new credit products.

According to the Federal Reserve’s 2023 Report on the Economic Well-Being of U.S. Households, 37% of Americans could not cover a $400 emergency expense with cash — making an emergency sinking fund the highest-priority line item in any new budget.

How Often Should You Review and Adjust Your Budget?

A monthly budget requires a weekly five-minute check-in and a full monthly review — not a set-it-and-forget-it approach. Most budgets drift off track within the first three weeks without any deliberate course correction.

The weekly check-in answers one question: am I on pace in each spending category, or do I need to shift money around? The monthly review is more comprehensive — comparing actual spending to planned spending, updating categories for the coming month, and adjusting for known changes like a rent increase or upcoming travel.

When to Rebuild Your Budget From Scratch

Certain life events warrant a full budget rebuild rather than an adjustment: marriage, divorce, a new child, a significant income change, or a major move. Use these transitions as a structured opportunity to reassess your financial goals. If you find that short-term goals keep collapsing after the first month, the issue is usually goal design — not willpower. Our article on financial goals that don’t fall apart after a month addresses that pattern directly.

Learning how to create a monthly budget is also the foundation for longer-term planning. Once your spending is under control, the next step is building toward bigger goals — whether that is investing in index funds or ETFs, or exploring what retirement actually costs so your savings targets are accurate.

“The budget review is where the real work happens. Tracking alone tells you where your money went. Reviewing tells you whether those decisions aligned with what actually matters to you.”

Frequently Asked Questions

How do I start a monthly budget with irregular income?

Use your lowest monthly income from the past six months as your baseline figure. Budget only from that conservative number, and treat any income above the baseline as a bonus to direct toward savings or debt. This method prevents overspending in high-earning months.

What is the easiest budgeting method for beginners?

The 50/30/20 rule is the easiest starting framework because it requires only three categories. Allocate 50% of net income to needs, 30% to wants, and 20% to savings and debt repayment. It is flexible enough to adjust as your financial situation becomes clearer.

How long does it take to create a working monthly budget?

The initial setup takes approximately 60 to 90 minutes — time spent pulling three months of bank and credit card statements, listing all expenses, and assigning category limits. The first three months are a calibration period where you refine categories based on actual behavior.

Should I use a budgeting app or a spreadsheet?

Apps are better for most people because automated transaction import removes the biggest barrier — manual data entry. YNAB, Monarch Money, and Mint (now discontinued but succeeded by similar tools) all connect to financial accounts directly. Spreadsheets work well for people who prefer full control and spend time regularly maintaining them.

How do I budget when I am living paycheck to paycheck?

Start by identifying your three largest discretionary spending categories and cutting each by 10–15%. Direct the difference to a $500 emergency fund first — this single buffer prevents most budget-breaking emergencies from becoming debt. Once that fund exists, begin addressing the structural causes of the paycheck-to-paycheck cycle.

What percentage of income should go to housing in a monthly budget?

Financial planners and the CFPB both recommend keeping housing costs at or below 30% of gross income. If housing exceeds 30%, you are classified as cost-burdened, and other budget categories — particularly savings — will need to be evaluated carefully.

How do I stay motivated to stick to my monthly budget?

Attach your budget to a specific, time-bound goal rather than a vague desire to “save more.” Research published by the American Psychological Association consistently shows that goal specificity increases follow-through rates. Review your stated goal every time you open your budget to reinforce the connection between daily decisions and long-term outcomes.