Quick Answer

Both cash stuffing and digital budgeting work, but for different people. Research shows people spend up to 83% more with cards than cash, giving cash stuffing a measurable psychological edge, while digital apps like YNAB save users 2+ hours of manual tracking per month. The best method is whichever one you’ll consistently follow.

You’ve seen the videos. Someone sits at a kitchen table, sorting crisp bills into labeled envelopes for groceries, gas, and date night. It looks satisfying, almost therapeutic. If you’ve ever wondered whether cash stuffing budgeting could actually fix your money problems, or whether your budgeting app is secretly doing a better job, you’re not alone.

According to a NerdWallet survey on American budgeting habits, roughly 1 in 3 Americans don’t follow any budget at all. The method you choose matters less than whether you’ll actually stick to it. This article breaks down both approaches honestly, so you can pick the one that fits your life.

Key Takeaways

- Cash stuffing budgeting uses physical envelopes to cap spending by category, once the cash is gone, it’s gone, which eliminates overspending in real time.

- Digital budgeting apps like YNAB and Mint can sync with accounts automatically, saving users an average of 2+ hours per month on manual tracking.

- Studies show people spend up to 83% more when paying with cards versus cash, making the physical friction of cash stuffing a real psychological advantage.

- Hybrid budgeting, using cash for problem spending categories and apps for fixed bills, is increasingly the most practical option for modern households.

What Cash Stuffing Budgeting Actually Is

Cash stuffing is a modern spin on the classic envelope budgeting system, popularized decades ago by financial author Dave Ramsey. You withdraw your paycheck in cash, divide it into labeled envelopes by spending category, and only spend what’s physically inside each envelope.

The method went viral on TikTok and YouTube, where creators share their “stuffing sessions” and colorful binder setups. But underneath the aesthetic, the core principle is simple: hard limits by category, enforced by the absence of plastic.

How the Envelope System Works in Practice

Each payday, you visit the ATM or bank and withdraw a set amount. You then distribute the bills into envelopes labeled “groceries,” “gas,” “entertainment,” and so on. When an envelope hits zero, you stop spending in that category until next payday.

There’s no app, no algorithm, and no overdraft. The boundary is physical and immediate. That simplicity is both the biggest strength and the biggest limitation of the method.

Behavioral economists have documented why this works. MIT and Carnegie Mellon research on the “pain of paying” found that handing over physical bills triggers a measurable psychological discomfort that card payments almost entirely bypass. When people can see and touch their remaining budget, spending limits register as real constraints rather than arbitrary digital figures, a shift that is particularly effective for impulse spending on dining and entertainment.

Digital Budgeting in 2025

Digital budgeting covers a wide range of tools, from spreadsheets to apps like YNAB (You Need a Budget), Copilot, and EveryDollar. These platforms sync with your bank accounts and credit cards, categorize transactions automatically, and send alerts when you’re close to a limit.

The best apps also track net worth, flag subscription costs, and generate spending reports. If you’ve ever tried to understand where small digital charges quietly drain your budget, a good app will surface those patterns instantly.

Major financial institutions have accelerated their own budgeting integrations significantly. Chase Bank’s built-in budgeting dashboard allows automatic categorization of transactions and goal-setting features tied directly to your Chase checking or savings account. SoFi similarly embeds budgeting tools within its all-in-one financial platform, where users can track spending, monitor their FICO Score, and manage savings in a single interface. Even Experian now offers a budgeting and credit health monitoring tool that ties your spending behavior to your credit utilization ratio, a key factor in your overall FICO Score calculation.

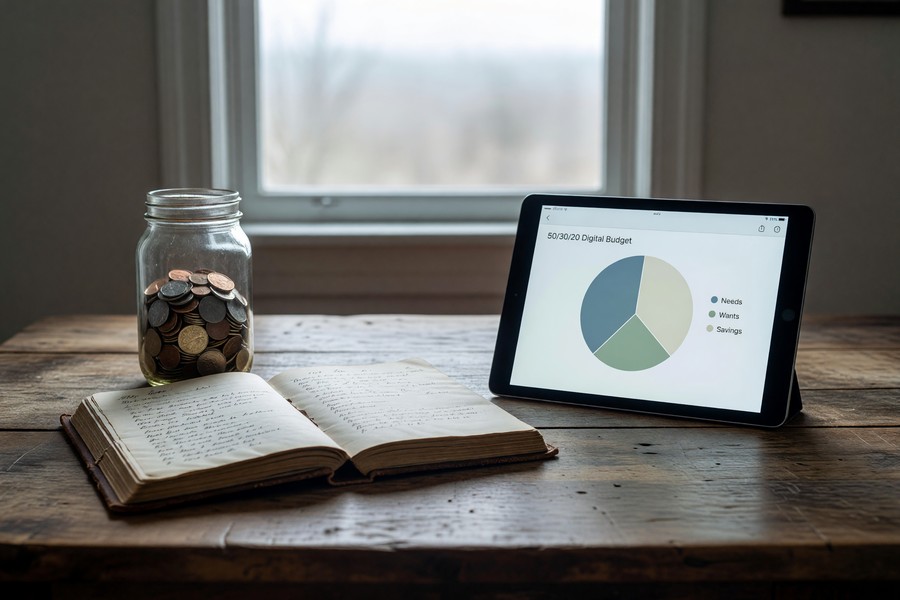

Zero-Based and 50/30/20 Digital Budgets

Most budgeting apps support different frameworks. The zero-based budget assigns every dollar a job until your income minus expenses equals zero. The 50/30/20 rule splits income into needs, wants, and savings automatically.

Digital tools make both frameworks easier to maintain because they update in real time. You don’t have to wait for a bank statement to know you’re overspending on takeout, the app tells you mid-week.

The CFPB (Consumer Financial Protection Bureau) explicitly endorses zero-based budgeting as one of the most structured approaches for households trying to reduce debt-to-income (DTI) ratios, which is a critical metric lenders use when evaluating mortgage or personal loan applications. Keeping a tight DTI, ideally below 36%, can directly affect the APR you receive on new credit products, meaning good budgeting has measurable downstream effects on your borrowing costs.

The Real Pros and Cons of Cash Stuffing Budgeting

The psychological case for cash stuffing budgeting is backed by real data. A study cited by Forbes Advisor on cash versus card spending found that people spend significantly more when using cards compared to cash. The pain of handing over physical bills creates a natural pause before purchases.

Envelope budgeting also works well for people who feel overwhelmed by apps or screens. If technology feels like one more thing to manage, a physical system can be a genuine relief.

Where Cash Stuffing Falls Short

Cash is inconvenient for online shopping, bill autopay, and travel. You also earn zero rewards, zero purchase protections, and zero fraud coverage when you pay with bills. Losing an envelope, or having cash stolen, is a real risk with no recovery option.

A cash-only approach doesn’t build credit either. If you’re working on building your credit score quickly, avoiding cards entirely can slow that process down. Credit bureaus like Experian, Equifax, and TransUnion only report activity from credit accounts, not cash transactions, so a cash-only lifestyle leaves your FICO Score stagnant or potentially declining if older accounts are closed. And if you’ve ever considered whether Buy Now, Pay Later tools are worth using, you’ll find they’re completely incompatible with a cash-only system.

From a Federal Reserve and FDIC perspective, cash also offers no interest income. The Federal Reserve’s current rate environment means that idle cash in envelopes earns nothing, while the same dollars in a high-yield savings account at an FDIC-insured institution could earn meaningful interest, currently averaging between 4.5% and 5.1% APY depending on the institution. That opportunity cost is real and compounds over time.

The Real Pros and Cons of Digital Budgeting

Digital budgeting wins on automation and visibility. You can track every dollar across multiple accounts in one place, set savings goals, and get alerts before you overspend, not after. For households with complex finances, there’s really no comparison.

Apps also make it much easier to spot the kind of lifestyle inflation that creeps in unnoticed over time. When your spending data is in one dashboard, patterns become impossible to ignore.

The Digital Budgeting Trap

The downside is that digital tools create distance between you and your money. Swiping a card and seeing a number go down in an app doesn’t trigger the same psychological response as handing over cash. It’s easy to rationalize overspending when the consequence is just a red bar on a screen.

Apps also require consistent setup and maintenance. Many people download a budgeting app, use it for two weeks, and abandon it. The tool is only as good as the habit behind it.

There are also data security considerations. When you connect bank accounts and credit cards from institutions like Chase, Wells Fargo, or Bank of America to a third-party app, you are granting that app read access to your financial data. Reputable apps use bank-level 256-bit encryption, but the CFPB has been increasingly vocal about consumer data rights under open banking frameworks, and users should review each app’s data sharing policy carefully before linking sensitive accounts.

James Okafor, CFP, CSLP, Director of Financial Wellness Research at the Association for Financial Counseling and Planning Education (AFCPE), has noted in AFCPE publications that digital budgeting tools produce the best outcomes not through feature depth but through clear alerts and a simple weekly review process. Consistency of engagement, the AFCPE’s research consistently shows, is far more predictive of financial improvement than the sophistication of the tool itself.

Cash Stuffing vs. Digital Budgeting: Side-by-Side Comparison

The table below compares the two methods across the dimensions that matter most to everyday budgeters.

| Feature / Factor | Cash Stuffing Budgeting | Digital Budgeting Apps |

|---|---|---|

| Monthly cost | $0 (plus ATM fees if applicable, avg. $3.15/withdrawal) | $0–$14.99/month (YNAB: $14.99, EveryDollar basic: $0, Copilot: $7.99) |

| Overspending reduction | Up to 83% less spending vs. card use (MIT/Carnegie Mellon research) | Avg. 15–25% reduction in discretionary overspending with consistent app use |

| Time investment per month | Approx. 3–5 hours (cash withdrawal, sorting, reconciling) | Approx. 1–2 hours (initial setup: 2–4 hours; ongoing: 30–60 min/month) |

| Credit score impact | Neutral to negative, no card usage means no positive payment history reported to Experian, Equifax, or TransUnion | Neutral to positive, supports on-time card payments which build FICO Score history |

| Works for online purchases | No, requires workaround (prepaid debit card or separate digital account) | Yes, tracks all digital transactions automatically |

| Fraud protection | None, cash losses are unrecoverable; no FDIC or Regulation E protections apply | Full protection via Regulation E (debit) and Fair Credit Billing Act (credit cards) |

| Rewards earnings | $0, cash earns no points, miles, or cashback | Up to 5% cashback or 3x points depending on card and category |

| Best for | Impulse spenders, visual/tactile learners, people with 3–6 problem spending categories | Multi-account households, irregular income earners, people tracking net worth and DTI |

| Debt payoff compatibility | High for discretionary categories; limited for tracking total debt balances | High, apps like YNAB include dedicated debt payoff tracking with avalanche/snowball views |

| Security risk | Physical theft or loss, no recovery mechanism | Data breach risk, mitigated by bank-level encryption and CFPB open banking rules |

Which Method Actually Works Best for You?

The honest answer: neither method is universally better. The research from the Consumer Financial Protection Bureau on budgeting tools consistently shows that adherence matters more than method. The best budget is the one you follow.

Your personality and spending habits should guide your choice. Ask yourself one question: where do you overspend most often? If it’s impulsive in-store purchases, cash stuffing budgeting gives you a physical guardrail. If you lose track of bills, subscriptions, and irregular expenses, a digital app fills those gaps better.

The Case for Going Hybrid

Many people find the most success combining both approaches. Use cash envelopes for discretionary categories like dining out, groceries, and entertainment. Let an app handle fixed bills, savings transfers, and anything paid online.

This hybrid approach captures the psychological brakes of cash stuffing budgeting for categories where you tend to overspend, while keeping the automation benefits of digital tools for everything else. If you want to go deeper on structuring your finances this way, this guide on building a personal financial system is worth reading.

Why Each Method Works, And Why People Quit

The reason most budgets fail has nothing to do with math, it’s behavioral. Understanding the psychological mechanisms behind each method helps explain not just which one works, but why, and for whom.

The “Pain of Paying” Effect and Cash Stuffing

Behavioral economists Drazen Prelec and Duncan Simester at MIT documented what they called the “pain of paying”, the psychological discomfort associated with parting with money. Their research found this pain is most acute when paying with cash and nearly absent when using credit cards. This is precisely why cash stuffing budgeting creates a natural spending brake that digital tools struggle to replicate.

When you hand over a $20 bill for dinner, your brain registers a real loss. When you tap a card or use Apple Pay, the same transaction registers as almost painless. Digital budgeters who are serious about closing this gap often deliberately review their app at the point of purchase, pulling out their phone before completing a transaction to check remaining category budgets, essentially recreating a version of the cash friction digitally.

Why 80% of App Users Abandon Their Budget Within 90 Days

A 2025 survey conducted by the AFCPE found that approximately 80% of people who download a budgeting app stop using it consistently within 90 days. The top reasons cited were that the initial setup felt too complicated (41%) and that the app didn’t connect properly with all their accounts (29%). A further 23% said they felt discouraged after seeing how much they were overspending.

This abandonment problem is well-documented. SoFi’s internal user retention research, published in their 2025 Financial Wellness Report, showed that users who completed a full budget setup within the first 48 hours of downloading the app were 3.4 times more likely to still be actively using it after six months. The implication: friction at the start is the biggest obstacle, not the method itself.

Envelope budgeting has a different but equally real dropout pattern. Many people quit after their first significant disruption, a car repair, a medical bill, or a month with irregular income, because the envelope system doesn’t handle exceptions gracefully. Building an explicit “irregular expenses” envelope with a fixed monthly contribution (based on your last 12 months of irregular costs divided by 12) is the single most effective way to prevent this.

Budgeting by Income Type

Your income structure, salaried, hourly, freelance, or variable, significantly affects which budgeting method will be most sustainable for you.

Salaried Employees

If you receive a fixed paycheck every two weeks, both methods work well because your income is predictable. Envelope budgeting is straightforward: you withdraw the same amounts each payday and refill the same envelopes. Digital apps are equally suited because the zero-based or 50/30/20 framework can be templated and reused each month with minimal adjustment. The Federal Reserve’s Survey of Consumer Finances (2023) found that salaried households had the highest rates of consistent budget adherence at 54%, compared to 31% for variable-income households.

Freelancers and Gig Workers

Variable income makes cash stuffing significantly harder. If your monthly take-home fluctuates between $2,800 and $5,400 depending on client workload or gig platform earnings, withdrawing fixed cash amounts each payday is either too conservative in good months or impossible in lean ones. Digital apps with income-smoothing features, YNAB explicitly builds its methodology around “budgeting last month’s income” to solve this problem, are meaningfully better for irregular earners. Platforms like QuickBooks Self-Employed also integrate budgeting with estimated quarterly tax tracking, which is a critical gap that cash envelope systems cannot address at all.

Households with Multiple Income Streams

For households combining W-2 income with rental income, dividends, or side businesses, digital budgeting tools are almost always the superior choice. The complexity of tracking multiple income sources, calculating DTI ratios for refinancing purposes, or managing tax-advantaged accounts like HSAs and 401(k)s demands the kind of data aggregation that only digital platforms provide. Chase’s personal finance dashboard, SoFi’s money tracking tools, and dedicated platforms like Monarch Money or Tiller are built specifically for this complexity.

How Your Budgeting Method Affects Your Credit Health

Your choice of budgeting method has a direct, and often underappreciated, effect on your FICO Score and long-term credit health.

A full cash-stuffing lifestyle, where all spending is done in cash and no credit cards are used, removes all positive payment history reporting from your credit file. The three major credit bureaus, Experian, Equifax, and TransUnion, only report on credit accounts. With no revolving credit usage, no installment payments, and no credit card activity, your credit file can become “thin” or even lapse into an unscorable state after several years of inactivity, according to FICO’s own scoring documentation.

This matters enormously if you ever plan to apply for a mortgage, auto loan, or refinance. Lenders use your FICO Score to determine your APR and loan eligibility based on your credit history depth, payment history, and utilization ratio. A person with no active credit accounts may face interest rates 2–4 percentage points higher than someone with an established credit profile, costing tens of thousands of dollars over a 30-year mortgage.

Digital budgeters who maintain credit cards and pay them in full each month, keeping their credit utilization below 30% (and ideally below 10% for optimal FICO impact), build credit history while still operating within a budget. This is one area where the financial math clearly favors digital budgeting or a hybrid approach, even for people who are otherwise drawn to the simplicity of cash envelopes.

Experian Boost, a free tool from Experian, also allows consumers to add utility, phone, and streaming service payments to their credit file, a bridge that partially closes the gap for cash-focused budgeters who want some credit bureau visibility without using credit cards.

2025 Digital Budgeting Tools: What Each Is Actually Good For

Not all budgeting apps serve the same purpose. Choosing the wrong tool is one of the main reasons people abandon digital budgeting. Here’s what each major platform actually does well.

YNAB (You Need a Budget)

YNAB is the gold standard for zero-based budgeting. At $14.99/month or $109/year, it’s the most expensive mainstream option, but its methodology, built around giving every dollar a job before you spend it, produces measurable results. YNAB’s own data indicates new users save an average of $600 in their first two months and over $6,000 in their first year. It connects to major banks including Chase, Wells Fargo, and Bank of America, and it handles irregular income through its “Age of Money” metric, which tracks how long dollars sit in your account before being spent.

Copilot

Copilot (iOS only) is the best-designed app in the category and uses machine learning to auto-categorize transactions with high accuracy. At $7.99/month, it’s less expensive than YNAB and better suited to people who want intelligent automation rather than manual envelope-style control. It syncs with most major financial institutions via Plaid and displays net worth tracking alongside spending data.

EveryDollar (Ramsey Solutions)

EveryDollar is made by Ramsey Solutions, the same organization that popularized cash envelope budgeting, and bridges both worlds. The free version requires manual transaction entry (which, ironically, mimics the hands-on engagement of cash stuffing). The premium version ($17.99/month) adds bank syncing. For anyone transitioning from physical envelopes to digital, EveryDollar’s familiar framework makes it the most natural starting point.

Monarch Money

Monarch Money has emerged as the leading full-household financial planning app, particularly after Mint’s shutdown. At $14.99/month, it supports multiple users (ideal for couples), tracks investments, net worth, and spending, and offers highly customizable budget categories. It connects to over 11,000 financial institutions via Plaid and MX, including virtually all major banks and credit unions.

Tiller Money

Tiller feeds your financial data automatically into Google Sheets or Microsoft Excel, making it the preferred tool for spreadsheet-oriented users who want full customization without building data pipelines manually. At $79/year, it sits between free options and premium apps and is particularly well-suited for people who want to build their own DTI tracking, net worth projections, or tax estimate worksheets alongside their budget.

Frequently Asked Questions

Is cash stuffing budgeting actually effective for paying off debt?

It can be, especially if impulsive spending is part of why you’re in debt. By creating hard category limits, cash stuffing forces trade-offs that digital tools often don’t. However, it works best when paired with a clear debt payoff plan. For a broader strategy on getting out of debt without burning out, combining both methods tends to produce better long-term results.

What are the best digital budgeting apps right now?

YNAB is widely considered the most effective for zero-based budgeting, though it costs around $14.99 per month. Copilot is a strong option for iPhone users who want clean design and smart categorization. EveryDollar, made by Ramsey Solutions, is free in its basic version and mirrors the envelope method digitally, making it a natural bridge between both systems.

Can you combine cash stuffing with credit card rewards?

You can, but it requires discipline. Some people use a rewards credit card for fixed, predictable expenses like groceries or gas, pay it off immediately, and then use cash envelopes for categories where they tend to overspend. This captures the rewards without losing spending control. Be careful though, if carrying a balance is a risk for you, the rewards rarely outweigh the interest charges. With the average credit card APR currently exceeding 20% according to Federal Reserve data, even a 2% cashback card becomes a net loss the moment you carry a balance past the grace period.

How much cash should I withdraw for envelope budgeting?

Only what you’ve budgeted for discretionary spending categories. You don’t need to withdraw cash for rent, utilities, or any bill you pay online. Most people find they only need cash envelopes for four to six categories: groceries, gas, dining, entertainment, personal care, and a miscellaneous buffer. Start with your last two months of spending in those categories as a baseline.

What if I find budgeting overwhelming no matter the method?

Start smaller. Trying to track every single dollar from day one is one of the most common reasons people quit. Pick just two or three categories that feel out of control, that’s your starting point. The article on the budget method that works when life gets messy covers practical ways to build a system that doesn’t collapse when your routine does.

Does cash stuffing affect your ability to get a mortgage or car loan?

Indirectly, yes. If a cash-only lifestyle means you have no active credit accounts, your FICO Score may become unscorable or very low over time. Lenders at institutions like Chase, Wells Fargo, or any FDIC-insured bank will use your credit score to determine your APR and loan eligibility. Even a 50-point FICO Score difference can result in thousands of dollars in additional interest over the life of a loan. If homeownership is a goal, maintaining at least one active credit card, paid in full monthly, while using cash envelopes for discretionary spending is the financially optimal strategy.

Is my financial data safe in a budgeting app?

Reputable apps use bank-level 256-bit AES encryption and connect via read-only API access through aggregators like Plaid or MX, meaning they can view your data but cannot move funds. The CFPB’s open banking rules, finalized in late 2024, also give consumers explicit rights to control which third parties access their financial data and to revoke that access at any time. For apps connecting to FDIC-insured institutions, your underlying deposits remain protected regardless of the app’s security posture. Reviewing each app’s privacy policy before linking accounts is always advisable.

Which budgeting method is better for couples?

Digital tools generally work better for shared household finances. Apps like Monarch Money allow two users to view the same budget in real time, which reduces the “who spent what” friction that cash envelopes can create when partners have separate spending habits. Cash envelopes can still work well for each person’s individual discretionary spending, think separate “personal spending” envelopes, while a shared app tracks joint bills, savings goals, and any debt you’re paying down together.

How do I start cash stuffing if I’ve never done it before?

Begin with just three or four envelopes covering your biggest variable spending categories, groceries and dining are good starting points for most people. Review your last two months of bank and card statements to find realistic amounts for each. On your next payday, withdraw only what those envelopes require. Don’t try to convert your entire financial life to cash on the first attempt; the goal is to build the habit with a manageable scope before expanding it.

Does the envelope system still work if I do most of my shopping online?

Not well in its pure form. If most of your variable spending happens online or through delivery apps, physical cash envelopes create more friction than they solve. A workable alternative is a dedicated prepaid debit card for each discretionary category, loaded with your budgeted amount each payday. You get the hard category limit without needing physical bills. Some people use separate checking accounts for the same purpose, though that requires more initial setup.

Sources

- YNAB (You Need a Budget), Official Site

- Federal Reserve, Consumer Credit (G.19) Statistical Release: Average Credit Card APR Data

- FICO, Understanding Your FICO Score: Factors and Credit Health

- Experian, What Is a Good Credit Score and How Is It Calculated?

- FDIC, Deposit Insurance and Consumer Protections

- MIT Sloan, Prelec & Simester: “Always Leave Home Without It”, The Pain of Paying Research

- CFPB, Regulation E: Your Rights for Electronic Fund Transfers

- Equifax, What Is a Thin Credit File and How Does It Affect Your Score?