Fact-checked by the Prime Rate editorial team

Quick Answer

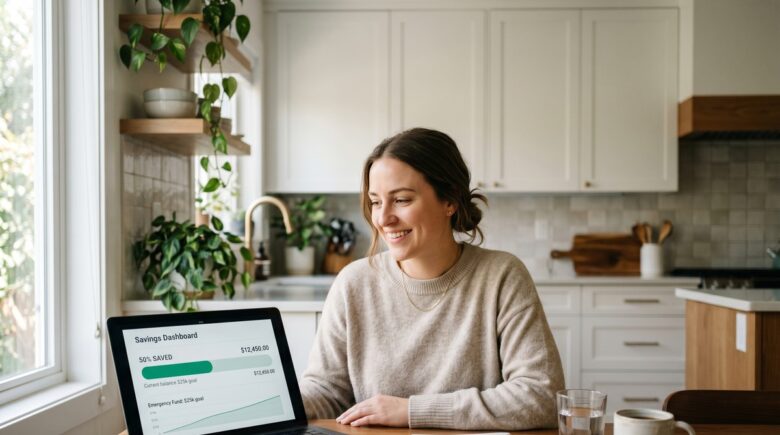

To build a six-month emergency fund, calculate your essential monthly expenses, multiply by six, and deposit the total into a high-yield savings account (HYSA) earning 4.50% APY or more. Top HYSAs pay significantly more than the national average savings rate of 0.41% APY, making them the optimal vehicle for this goal.

The national average savings account rate sits at just 0.41% APY, according to FDIC data. Parking emergency cash at that rate while high-yield alternatives exist is a straightforward opportunity cost — one that compounds against you every month you wait. A household with $19,200 in a standard savings account earns roughly $79 per year in interest. The same balance in a top-tier HYSA at 4.50% APY earns closer to $864.

With the Federal Reserve holding rates elevated, top online banks are offering HYSA yields that have not been this attractive since before the 2008 financial crisis. The right account paired with a consistent deposit plan makes the difference between a fund that stagnates and one that builds real momentum.

Key Takeaways

- The national average savings account rate is 0.41% APY, according to the FDIC — top HYSAs pay more than ten times that rate.

- 37% of U.S. adults could not cover a $400 emergency with cash, per the Federal Reserve’s 2023 Household Well-Being Report, making an emergency fund the highest-priority personal finance step before investing.

- The CFPB recommends three to six months of essential expenses, with six months as the standard for single-income households and those with variable pay.

- Top-tier HYSAs are currently offering 4.25%–5.00% APY, while 12-month CDs range from 4.50%–5.10% APY — but CDs are unsuitable as a primary emergency account due to withdrawal penalties.

- The Prime Rate of 7.50% is the direct mechanism keeping HYSA yields elevated; a Federal Reserve rate cut will compress those yields, typically within days of the Fed’s announcement.

- Automating a fixed transfer on payday is the single most reliable behavior for reaching a savings goal — the amount matters less than the consistency, especially in early stages.

How Much Do You Actually Need in a Six-Month Emergency Fund?

Your target is six times your essential monthly expenses, not your income. Start by listing only non-negotiable costs: rent or mortgage, utilities, groceries, insurance premiums, minimum debt payments, and transportation. Discretionary spending like dining out or subscriptions is excluded from the calculation.

If your essential monthly expenses total $3,200, your six-month target is $19,200. The Consumer Financial Protection Bureau (CFPB) recommends three to six months of expenses as a baseline, with six months being the standard for households with variable income, dependents, or a single earner. For dual-income households with stable employment, three to four months may be sufficient — but six months is the conservative, broadly applicable target.

Using income rather than expenses is the most common calculation error. If you earn $6,000 per month but only spend $3,200 on essentials, your target is $19,200 — not $36,000. Overshooting the target means money that could be invested or used for debt repayment sits in a savings account doing less work than it should.

Expense Categories to Include in Your Baseline

Your baseline calculation should cover housing, food, utilities, healthcare premiums, minimum loan payments, and essential transportation. Exclude retirement contributions, entertainment, and savings transfers — those pause during a genuine emergency. Building this budget first is the same discipline covered in our guide on how to create a monthly budget that actually works.

One category people frequently undercount is insurance. Health, auto, and renters or homeowners premiums continue regardless of employment status. If you carry a monthly car payment, that minimum payment belongs in the baseline too. Healthcare out-of-pocket costs are harder to predict, but including your monthly premium and a modest buffer is reasonable.

When Six Months May Not Be Enough

Self-employed workers, freelancers, and commission-based earners should consider targeting nine to twelve months. Income volatility in those situations means a six-month buffer can be consumed faster than expected. The same logic applies to households in industries with cyclical layoffs or those carrying significant fixed liabilities like a mortgage in a market where selling quickly is not realistic.

Key Takeaway: Multiply your essential monthly expenses by six to set your exact savings target. The CFPB recommends six months as the benchmark for single-income households and those with variable pay — discretionary spending is excluded from the calculation.

Which High-Yield Savings Account Is Best for an Emergency Fund?

The best account combines a high APY, FDIC insurance, zero monthly fees, and fast access to funds. Online banks and credit unions consistently outperform traditional brick-and-mortar institutions on all four criteria, primarily because they carry lower overhead costs and pass those savings to depositors.

Top-tier HYSAs — including those from institutions like Marcus by Goldman Sachs, Ally Bank, SoFi, and Discover Bank — are offering rates between 4.25% and 5.00% APY. Our ranked list of the best high-yield savings accounts for 2026 compares current rates and account features side by side.

HYSA vs. Money Market Account vs. CD

A money market account (MMA) offers similar yields with check-writing privileges, but may require higher minimum balances. A certificate of deposit (CD) locks funds for a fixed term, making it unsuitable as your primary emergency account — early withdrawal penalties typically run 90 to 180 days of interest, which defeats the purpose of liquid emergency savings. For liquidity combined with yield, an HYSA is the right first choice. Our comparison of CD rates vs. high-yield savings covers the trade-offs in depth.

| Account Type | Typical APY | Liquidity | Best For |

|---|---|---|---|

| High-Yield Savings | 4.25%–5.00% | Immediate (2–3 days transfer) | Primary emergency fund |

| Money Market Account | 4.00%–4.75% | Immediate (check/debit access) | Emergency fund with check access |

| Traditional Savings | 0.01%–0.50% | Immediate | Not recommended for this goal |

| 12-Month CD | 4.50%–5.10% | Locked (penalty to withdraw) | Supplemental savings only |

| Checking Account | 0.01%–0.10% | Instant | Bill payments, not savings |

What to Look for Beyond the APY

APY is the headline number, but it is not the only number that matters. Confirm the account carries no monthly maintenance fees, since a $10 monthly fee erases a meaningful portion of interest earned on a small balance. Check the transfer speed: most online HYSAs settle transfers in two to three business days, but some institutions offer same-day or next-day options for linked accounts.

Also verify whether the advertised rate is a promotional introductory rate or the ongoing rate. Some banks offer elevated rates for the first three to six months, then step down. For an emergency fund with a multi-year savings horizon, the ongoing rate is what matters.

Key Takeaway: Top high-yield savings accounts are paying 4.25%–5.00% APY — more than ten times the national average. The best HYSAs combine FDIC insurance, no fees, and same-week liquidity, making them the only appropriate vehicle for a primary emergency fund.

How Do You Build a Six-Month Emergency Fund From Scratch?

Build a six-month emergency fund through three sequential steps: set your target, automate consistent deposits, and remove the friction that causes people to stop contributing. Speed matters less than consistency. A sustainable $200 monthly contribution beats a $1,000 burst that depletes willpower and gets abandoned after two months.

Start with a seed deposit of at least $500 to open the account and establish a real balance. From there, set up an automatic transfer from your checking account on the day after your paycheck arrives. The Federal Reserve’s 2023 Report on the Economic Well-Being of U.S. Households found that 37% of adults could not cover a $400 emergency expense with cash. That figure puts the stakes in context: this fund is the highest-priority personal finance move before investing, before extra debt payments on low-interest loans, before almost anything else.

How Long Will It Take?

If your target is $18,000 and you save $600 per month at 4.50% APY, you reach your goal in approximately 28 months and earn roughly $1,100 in interest along the way. Increasing monthly contributions even modestly compresses that timeline significantly. Saving $900 per month instead brings the timeline down to about 19 months on the same target. Use windfalls — tax refunds, bonuses, side income — to accelerate progress without disrupting your regular budget.

The interest itself becomes a meaningful accelerant over time. At $10,000 saved, a 4.50% APY account generates roughly $38 per month in interest. That is not life-changing, but it does mean every month after the halfway mark, your account is contributing to its own completion.

The Psychology of Staying Consistent

Most people who fail to build an emergency fund do not fail because of math. They fail because the goal feels abstract until it is nearly complete. Two tactics help. First, name the account something specific in your bank’s interface — “Job Loss Fund” or “Six-Month Safety Net” performs better psychologically than a generic savings label. Second, treat the automatic transfer as a fixed expense rather than a discretionary savings decision. When it moves before you see the money, you stop negotiating with yourself about it every month.

Key Takeaway: Automating a fixed transfer on payday is the single most effective behavior to build a six-month emergency fund. The Federal Reserve found that 37% of U.S. adults lack the liquid savings to absorb a $400 shock — making automation the difference between a plan and a result.

How Do You Accelerate Your Emergency Fund Without Overhauling Your Budget?

Incremental changes to existing cash flow are more durable than dramatic budget cuts. The goal is to find money that is already moving through your life and redirect part of it before it gets absorbed into routine spending.

Tax refunds are the most reliable windfall most households receive. The IRS reports that the average federal tax refund has consistently exceeded $2,800 in recent years. Depositing that directly into your HYSA rather than routing it through checking reduces the chance it gets spent before you act. The same logic applies to annual bonuses, overtime pay, and any one-time income from selling items, freelance projects, or referral bonuses.

The “One Bill” Strategy

Rather than cutting across multiple spending categories simultaneously — which creates deprivation fatigue — identify one recurring subscription or service you can cancel or downgrade for a defined period. The $15 to $50 in monthly savings from a single decision is not dramatic, but it is sustainable. Add that amount to your automatic transfer and leave it there.

Side Income as a Savings Accelerant

Side income is most effective for emergency fund building when 100% of it is pre-committed to the goal. Designating a separate income stream entirely to the fund, rather than mixing it with general income, creates a clean psychological boundary. When the fund is complete, that income stream can be redirected. Many people find the focused purpose keeps them motivated to maintain the side activity long enough to reach the goal.

What Are the Most Common Emergency Fund Mistakes?

The most damaging mistake is keeping the fund in a checking account or a traditional savings account earning 0.01% to 0.50% APY. The difference in annual interest between a traditional savings account and a top HYSA on a $15,000 balance is roughly $600 to $700 per year. That money requires no additional work — it is purely a function of which account holds the balance.

The second most common error is treating the emergency fund as a flexible savings pool. Withdrawing from it for non-emergencies — a vacation, a sale purchase, a minor car repair that could be covered by current income — undermines both the balance and the habit. Define what qualifies as an emergency before you need to make that decision. Job loss, medical costs not covered by insurance, essential home or car repairs that affect safety: these qualify. A flight deal does not.

Investing the Emergency Fund for Higher Returns

Some people, frustrated by the gap between HYSA rates and stock market returns, consider putting their emergency fund into index funds or ETFs. This is a structural mistake. A brokerage account is not a liquid account in any practical sense during a real emergency. Markets can be down 20% or more precisely when a job loss or health crisis forces you to sell. The purpose of the emergency fund is to be stable and accessible, not to maximize returns. The CFP Board’s consumer research is consistent on this point: liquidity, not yield, is the defining requirement for emergency savings.

A high-yield savings account earning 4.50% APY is not a compromise. At current rates, it is a genuinely competitive return for a fully liquid, FDIC-insured account.

Key Takeaway: Keeping an emergency fund in a low-yield checking or traditional savings account costs hundreds of dollars per year in foregone interest. Investing the fund in equities introduces sequence-of-returns risk at exactly the wrong moment. A top HYSA resolves both problems. See our ranked HYSA list for current rates.

What Do You Do After Reaching Your Emergency Fund Goal?

Once you hit your six-month target, stop adding to the emergency fund and redirect contributions to wealth-building accounts. The emergency fund has a defined ceiling. It should not become a savings account you keep topping off indefinitely while delaying investing.

The sequence prioritized by most Certified Financial Planners (CFPs) is: maximize your 401(k) employer match first (it represents an immediate 50% to 100% return on those dollars), then fund a Roth IRA or Traditional IRA, then increase 401(k) contributions to the annual limit. For a deeper look at that decision, see our comparison of Roth IRA vs. Traditional IRA in 2026. Any remaining surplus can go into taxable brokerage accounts or a CD ladder strategy for medium-term goals.

Maintaining the Fund Over Time

Review your target annually. If your essential expenses rise — new rent, a car payment, a new dependent — recalculate your six-month number and adjust. After any drawdown, replenish the fund before resuming investing contributions. Treat it as a fixed balance to maintain rather than a flexible pool to borrow from.

Inflation also erodes the real value of a static fund over time. A $19,200 target that was accurate two years ago may represent only five months of expenses today if costs have risen. The annual review is not optional; it is part of what keeps the fund functional.

Key Takeaway: Once your six-month target is funded, redirect savings to tax-advantaged accounts. Capturing a full 401(k) employer match delivers an immediate 50%–100% return — a priority that outranks any additional emergency savings beyond your defined target. Revisit 2026 401(k) contribution limits to maximize the next step.

How Does the Prime Rate Affect Your Emergency Fund Yield?

The Prime Rate directly influences the APY that high-yield savings accounts pay. When the Federal Reserve raises the federal funds rate, the Prime Rate rises with it, and online banks typically pass those increases to depositors within days. The reverse is also true: when the Fed cuts rates, HYSA yields fall.

The Prime Rate currently stands at 7.50%, keeping HYSA yields elevated compared to the 2010–2021 near-zero rate environment. Understanding what happens to your savings when the Prime Rate rises helps you anticipate yield changes and decide when to lock in rates via a CD before the Fed pivots.

If rate cuts materialize, HYSA yields will compress. The emergency fund’s purpose remains unchanged regardless of rate direction — but for savings beyond your six-month target, a CD can preserve today’s returns before a cut takes effect. The core emergency fund should stay liquid regardless.

Key Takeaway: The Prime Rate of 7.50% is the reason top HYSAs pay over 4.50% APY. If the Fed cuts rates, yields will fall — locking a portion of surplus savings into a high-rate CD before a cut preserves today’s returns without sacrificing liquidity on your core emergency fund.

Frequently Asked Questions

How much should a six-month emergency fund be for the average American?

Multiply your monthly essential expenses by six. For a household with $3,500 in monthly essential expenses, the target is $21,000. Use actual expenses — not income — and exclude discretionary spending from the baseline calculation.

Is a high-yield savings account FDIC insured?

Yes. Any HYSA at an FDIC-member bank is insured up to $250,000 per depositor, per institution. Credit union equivalents are insured by the National Credit Union Administration (NCUA) under the same limits. Always verify membership before opening an account.

Should I pay off debt before building an emergency fund?

Build a small starter emergency fund of $1,000 first, then aggressively pay down high-interest debt. Once high-rate debt is cleared, redirect payments toward completing the full six-month fund. Carrying both goals simultaneously stretches resources too thin for most households.

Can I use a money market account instead of a high-yield savings account?

Yes. A money market account is a strong alternative, often offering check-writing and debit access that an HYSA lacks. Rates are comparable. The key criteria are FDIC or NCUA insurance, no monthly fees, and a yield above 4.00% APY at current rates.

What happens to my emergency fund if the Fed cuts interest rates?

Your HYSA yield will decline, but the fund’s value does not decrease — only the interest earned going forward drops. Maintaining the fund in a liquid account remains correct regardless of rate direction. Consider moving excess savings beyond your six-month target into a CD to lock in current rates before cuts occur.

How do I build a six-month emergency fund if I live paycheck to paycheck?

Start with whatever you can automate — even $25 per paycheck. The automation habit matters more than the amount in early stages. Simultaneously audit your budget for one or two recurring expenses to cut, and apply any tax refund, bonus, or side income directly to the fund before it reaches your checking account.