Fact-checked by the Prime Rate editorial team

Quick Answer

Multi-generational estate planning and wealth transfer requires moving beyond a simple will to a structure built on trusts, lifetime gifting, and family governance. Without a deliberate plan, roughly 70% of family wealth is lost by the second generation. Effective transfer uses tools like dynasty trusts and annual gift exclusions to move $124 trillion in projected U.S. wealth to heirs over coming decades while minimizing repeated taxation and family conflict.

The core of estate planning and wealth transfer isn’t about dodging taxes alone. It’s about ensuring what you’ve built actually survives you and the next generation. Most families blow it. Industry estimates consistently show that approximately 70% of family wealth disappears by the second generation, and up to 90% by the third. That’s not mainly because of estate taxes. It’s the slow erosion of unprepared heirs, family infighting, and a lack of clear instructions. The U.S. is currently in the middle of what Cerulli Associates calls the “Great Wealth Transfer,” with an estimated $124 trillion set to change hands from 2024 through 2048, of which $105 trillion will go to heirs.

This transfer is accelerating. A 2026 study from Bank of America Private Bank found that 23% of wealthy business owners now report inheriting their business, a sharp jump from 11% in 2024. Longevity is reshaping everything. 92% of wealthy Americans now say longevity is a critical factor in their financial planning, according to the same 2026 Bank of America study. That means more overlapping generations, more confusion, and more at stake.

This guide is for anyone holding assets they want to last past their children’s lifetimes, including business owners, parents of adult children, and people blending families. By the end, you’ll have a clear action plan for selecting trusts, communicating with heirs, and locking in tax advantages before the law changes.

Key Takeaways

- An estimated 70% of family wealth is lost by the second generation, with poor communication and lack of preparation as the primary drivers, not estate taxes alone.

- The total U.S. wealth transfer from 2024 through 2048 is projected at $124 trillion, with $105 trillion flowing directly to heirs, according to Cerulli Associates.

- Inherited business ownership jumped to 23% of wealthy respondents in 2026, up from 11% in 2024, signaling a major intergenerational shift in business succession, per the Bank of America Private Bank study.

- The federal estate and gift tax exemption sits at $13,990,000 per individual for 2025, allowing most families to focus on control and protection strategies even without a looming estate tax bill, per the IRS.

- 78% of wealthy business owners say succession planning is important, yet only 20% have a fully documented plan, creating an urgent gap between intention and action, according to the Bank of America Private Bank study.

- Coordinating dynasty trusts with retirement accounts and 529 plans can create layered, multi-generational tax benefits that a basic will cannot achieve.

In This Guide

- Step 1: How Do I Start Planning for Multi-Generational Wealth Transfer?

- Step 2: Which Trusts Actually Work for Passing Wealth to Grandchildren?

- Step 3: Should I Gift Assets Now to Reduce My Taxable Estate?

- Step 4: How Do I Communicate the Plan Without Sparking Family Conflict?

- Step 5: What Happens to IRAs and 401(k)s Across Generations?

- Step 6: How Do I Transfer a Family Business Without Breaking It?

- Step 7: What Are the Biggest Mistakes That Undo Multi-Generational Plans?

- Frequently Asked Questions

Step 1: How Do I Start Planning for Multi-Generational Wealth Transfer?

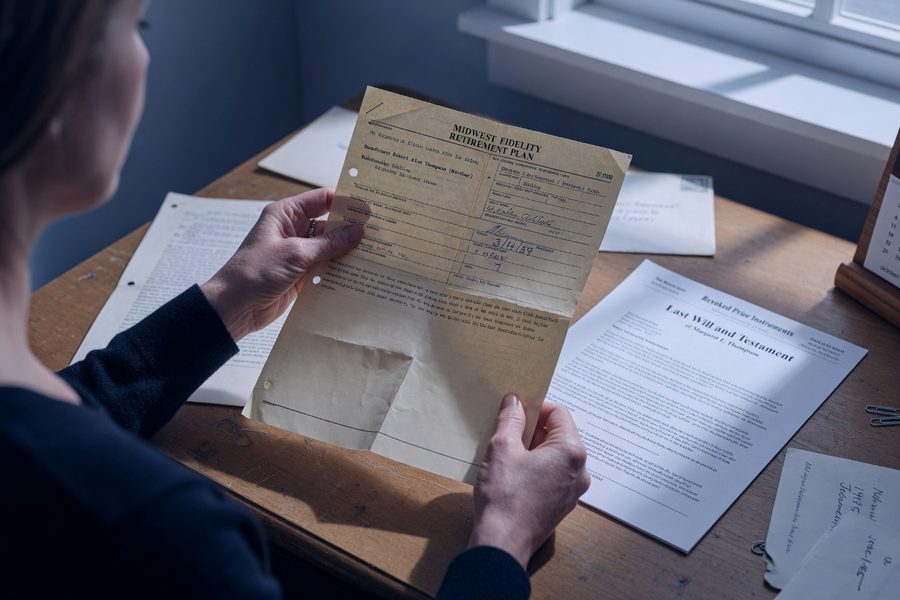

Start with a net worth statement that separates assets by how they transfer at death, probate assets, beneficiary-designated assets, and jointly held property. Estate planning and wealth transfer fails most often not from a missing document, but from a mismatch between what you own and how it’s titled. Pull every account statement, deed, and policy. List each asset, its current value, and exactly who inherits it under your current setup.

How to Do This

Open a spreadsheet. Create three columns: Asset, Current Ownership Structure, and Default Transfer Method. The IRS defines your gross estate as everything you own or hold an interest in at death. That includes real estate, cash, investments, business interests, and certain trusts. You need to know which of these will require probate, which bypass it via beneficiary designations, and which are already inside an irrevocable trust.

If you have a high net worth but haven’t updated beneficiary forms since opening accounts in your 30s, you are not alone. 78% of wealthy business owners say succession planning is important, but only 20% have a fully documented plan. Your first action is closing that gap between intention and paperwork.

What to Watch Out For

Beneficiary designations override your will. That means the retirement account you named your sibling on 15 years ago goes to them, even if your will says it goes to your spouse. Check every single designation now. Also watch for assets titled “jointly with rights of survivorship,” which automatically pass to the co-owner and bypass any trust structure you may later create.

Use a free tool like a state bar association’s estate planning checklist or meet with a Certified Financial Planner (CFP) for a one-time asset inventory session. Getting the inventory right often costs less than fixing a botched transfer later.

Step 2: Which Trusts Actually Work for Passing Wealth to Grandchildren?

A revocable living trust avoids probate but does nothing for generation-skipping transfer tax or asset protection. For true multi-generational estate planning and wealth transfer, you need irrevocable trusts, specifically dynasty trusts that use your generation-skipping transfer (GST) tax exemption. A dynasty trust holds assets for grandchildren and beyond, shielding the principal from estate taxes at each successive generation. The federal GST exemption amount matches the estate tax exemption: $13,990,000 per person in 2025, according to the IRS.

How to Do This

Work with an attorney who regularly drafts irrevocable trusts, not a general practitioner. Fund a dynasty trust with assets expected to appreciate significantly, like a family business interest or a portfolio of index funds. Allocate your GST exemption to the trust on a timely filed gift tax return. The trust can then distribute income to your children and principal to grandchildren, all outside their taxable estates. This is how families preserve wealth across three or more generations without a massive tax haircut each time someone dies.

What to Watch Out For

Dynasty trusts are permanent. Once assets go in and you allocate GST exemption, you can’t pull them back. Choose a trustee carefully; many families now opt for a corporate co-trustee to handle administrative complexity. State law limits on trust duration vary. Some states, like South Dakota and Delaware, permit perpetual trusts; others cap them at around 90 years. Your choice of trust situs matters enormously.

| Trust Type | Probate Avoidance | Multi-Gen Tax Shield | Asset Protection |

|---|---|---|---|

| Revocable Living Trust | Yes | No | No |

| Dynasty Trust (Irrevocable) | Yes | Yes | Yes |

| Testamentary Trust (in Will) | No | Partial (GST election at death) | After death only |

Step 3: Should I Gift Assets Now to Reduce My Taxable Estate?

Yes, if you can afford to part with the assets permanently. The math is straightforward: every dollar you give away during life, and its future appreciation, exits your taxable estate forever. The IRS sets an annual gift tax exclusion of $18,000 per recipient for 2025, allowing a married couple to transfer $36,000 per child or grandchild tax-free each year without touching their lifetime exemption. Over a decade, that’s $360,000 removed from an estate per recipient, before counting any growth.

How to Do This

Prioritize gifting appreciating assets with high basis. A share of a family business or a rental property placed in an irrevocable trust now locks in today’s valuation for gift tax purposes while all future growth happens outside the estate. You can also use a spousal lifetime access trust (SLAT) if you want to remove assets from your estate while retaining indirect access through your spouse’s beneficiary interest. File Form 709 with the IRS for any gift exceeding the annual exclusion.

The IRS describes the estate tax as a tax on your right to transfer property at your death, encompassing everything you own or have certain interests in at the date of death. Lifetime giving shifts that calculation by removing assets and their future growth from the equation before death ever occurs.

What to Watch Out For

Do not gift assets you might need. This sounds obvious, but families get aggressive with tax planning and then face a liquidity crisis in retirement. Gifting also carries basis over to the recipient, meaning they inherit your cost basis rather than getting a step-up at death. For highly appreciated stock you bought at $10 a share, a lifetime gift may saddle the recipient with a capital gains tax bill you could have avoided by holding until death.

Lifetime gifts eliminate the step-up in basis heirs receive when assets pass at death. Run the math on both the estate tax savings and the capital gains tax consequence before transferring appreciated securities.

Step 4: How Do I Communicate the Plan Without Sparking Family Conflict?

Start holding structured family meetings that separate values from dollars. The single biggest predictor of a failed wealth transfer isn’t a bad trust; it’s surprise and resentment among heirs. Families who incorporate behavioral coaching or third-party facilitators report measurably lower dispute rates. An open conversation about why the trust says what it says often diffuses the anger before it hardens into litigation.

How to Do This

Hire a facilitator: your estate attorney, a family therapist experienced in wealth counseling, or a CFP. Hold a meeting that covers three things: the family’s core values around money, an educational overview of the trust structure without dollar amounts, and a clear explanation of the roles (trustee, beneficiary, protector). If philanthropy is part of the plan, involve heirs in the grantmaking decisions through a donor-advised fund so the next generation practices stewardship before inheriting control.

What to Watch Out For

Do not spring the plan on your kids at Thanksgiving. One loaded dinner-table reveal does more damage than no communication at all. Also, avoid giving one child control over a sibling’s distribution without a clear rationale. Perceived favoritism in trustee selection is the most common trigger of trust litigation among siblings. Put the rationale in a non-binding letter of wishes.

Step 5: What Happens to IRAs and 401(k)s Across Generations?

The SECURE Act eliminated the “stretch IRA” for most non-spouse beneficiaries. Now, most heirs must empty an inherited IRA within 10 years, compressing the income tax hit. This change makes Roth conversions a powerful multi-generational tool. Pay the tax now, and your heirs get tax-free withdrawals.

How to Do This

Convert traditional IRA assets to a Roth IRA in years when your income is lower. Name a see-through trust as the IRA beneficiary to control distributions to heirs while preserving the 10-year payout rule. Coordinate Roth conversions with both your income tax bracket and the potential sunset of the Tax Cuts and Jobs Act provisions, which could raise rates. Every dollar converted at a 24% rate today is a dollar your heirs will not pay tax on at possibly higher rates.

For families with 529 college savings plans, consider naming a dynasty trust as the successor owner. Unused 529 funds can now be rolled into a Roth IRA for the beneficiary under certain conditions, creating a multi-generational education-to-retirement pipeline.

Most articles mention dynasty trusts but rarely detail how to coordinate them with retirement accounts or 529 plans for layered tax benefits across generations. Naming a trust as an IRA beneficiary is technically complex; do it wrong and the entire IRA becomes taxable immediately.

Step 6: How Do I Transfer a Family Business Without Breaking It?

Separate ownership from management before you die. A business that depends entirely on the founder’s relationships and knowledge will collapse; transferring that business to children who have never run anything is a recipe for failure. The Bank of America Private Bank study shows 23% of wealthy business owners now report inheriting their business, but the real risk is that the remaining 77% must sell or close because no succession plan exists. Only 20% have a fully documented succession plan.

How to Do This

Transfer non-voting equity into a dynasty trust now while you retain voting control. Use a grantor retained annuity trust (GRAT) to pass future appreciation to heirs with minimal gift tax consequences. Bring the next generation into management roles for a defined, mentored period, five years minimum, before handing over any voting control. This is not about fairness; it’s about survival. A child uninterested in the business should receive other assets instead of a management role they’ll resent.

What to Watch Out For

Do not split ownership equally among children who have unequal involvement. The child running the business needs both authority and a compensation structure that recognizes their work. Siblings who sit on the board but don’t work the day-to-day can be given dividend rights without operational control. Write the operating agreement as if the siblings will someday disagree, because they will.

78% of wealthy business owners say succession planning is important to their wealth strategy. Only 20% have a fully documented plan. That gap represents trillions of dollars moving through unprepared structures.

Step 7: What Are the Biggest Mistakes That Undo Multi-Generational Plans?

Relying on a basic will to transfer complex assets is the most common and costliest mistake. A will alone guarantees probate, public records, and no protection from creditors or divorcing spouses of heirs. For blended families, a will that hasn’t been updated since a second marriage can disinherit children unintentionally. The IRS notes that gift and estate taxes apply to transfers of money, property, and other assets under specific rules, rules that a simple will ignores entirely.

How to Do This

Review every document every three years, or immediately after a major life event: divorce, remarriage, birth of a child or grandchild, or a significant change in net worth. For blended families, use a qualified terminable interest property (QTIP) trust to provide for a surviving spouse while preserving the principal for children from a prior marriage. For digital assets like cryptocurrency, maintain an encrypted inventory of wallet addresses and private keys with explicit instructions in a side letter to your executor, courts still struggle with crypto in probate.

What to Watch Out For

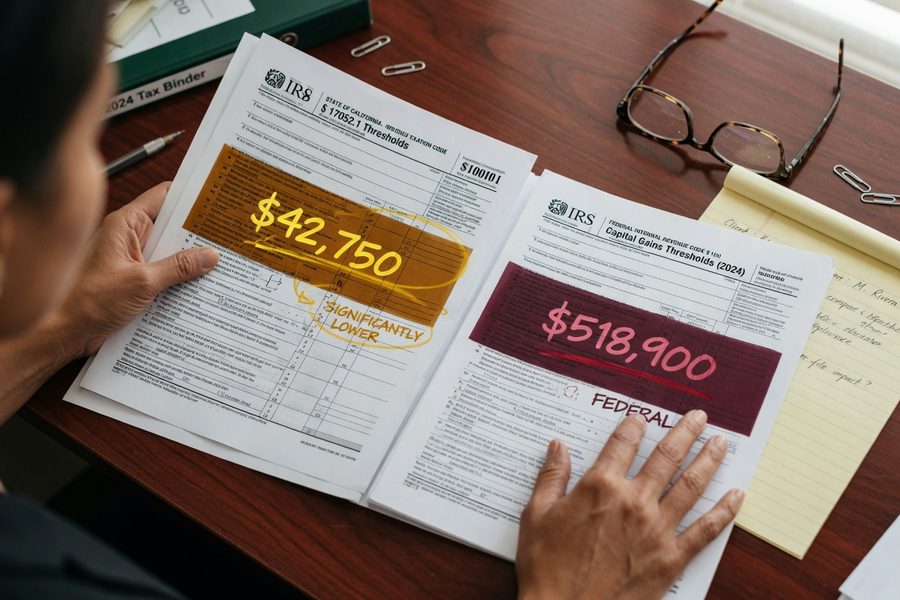

State estate taxes hit much lower thresholds than federal taxes. Just as a good credit score unlocks better loan terms, understanding your state’s estate tax rules unlocks planning opportunities. Massachusetts and Oregon tax estates over $2 million. New York’s cliff means an estate just over the exemption can face a crushing marginal rate. If you live in a high-tax state, the conversation shifts from “do I owe federal estate tax?” to “how do I avoid a state-level confiscation?” Coordinate your federal strategy with state-specific planning. This is an area most generic estate planning guides skip entirely.

Coordinate dynasty trusts with existing retirement accounts and 529 plans for layered tax benefits. For example, a dynasty trust holding a Roth IRA that names a 529 as the contingent beneficiary creates a multi-generational education and retirement pipeline that a basic will simply cannot replicate.

Frequently Asked Questions

What’s the difference between a revocable trust and an irrevocable trust for passing money to my grandkids?

A revocable trust avoids probate but offers zero tax or asset protection for your grandchildren. An irrevocable trust, like a dynasty trust, removes assets from your estate entirely and shields them from estate taxes at each successive generation, provided you allocate your GST exemption correctly. The trade-off is permanent loss of control; once assets go into an irrevocable trust, you can’t take them back.

Can I still do multi-generational planning if my total estate is under the federal exemption amount?

Yes. With the federal exemption at $13,990,000 per individual in 2025, most families won’t pay federal estate tax. But dynasty trusts offer asset protection against creditors, divorcing spouses of your heirs, and spendthrift beneficiaries. Control and protection are valid reasons to plan, even without a tax bill looming.

How do I deal with one child who is responsible with money and another who isn’t when I’m designing an inheritance plan?

Use a trust with an independent trustee and a distribution standard that ties payouts to specific milestones, college graduation, sustained employment, or reaching a certain age, rather than a lump sum at death. For the responsible child, you might grant co-trustee powers at a designated age. For the struggling child, the independent trustee retains discretion longer. A clear letter of wishes explains the reasoning without creating a legal entitlement either child can challenge.

How do I protect my kids’ inheritance from their future divorces?

An irrevocable trust with spendthrift provisions keeps inherited assets separate from marital property. If your child receives a direct inheritance and then commingles it in a joint account with their spouse, that money becomes divorce bait. A properly drafted dynasty trust keeps the assets titled in the trust’s name, not your child’s, so family law courts cannot divide it. Most families don’t think about this until the divorce papers arrive.

Are digital assets like crypto included in multi-generational estate plans?

They must be, but most estate attorneys are still catching up. Crypto held in a personal wallet passes to your estate like any other property, but without a clear inventory of wallet addresses and private keys, those assets are effectively lost. Use an encrypted password manager with detailed instructions in a side letter to your executor. For larger crypto holdings, consider placing them in a Wyoming or South Dakota trust specifically designed for digital assets. Do not assume your executor knows how to access or value cryptocurrency, they almost certainly do not.

How early should I teach my kids about money and wealth so it doesn’t ruin them?

Start in middle school with budgeting and compound interest, then phase in broader wealth concepts by high school. Families with higher retention rates across generations introduce heirs to philanthropic decision-making and investment basics long before any control is handed over. Concepts like maximizing an employer 401(k) match are foundational financial habits that build stewardship muscle. The goal isn’t to produce miniature portfolio managers; it’s to build the muscle of deferred gratification and responsibility before real money enters the picture.

What’s the biggest mistake people make with estate planning and wealth transfer when a second marriage is involved?

Failing to update beneficiary designations and trusting that a will covers everything. In blended families, a QTIP trust is often the right tool: it provides income to the surviving spouse for life while preserving the principal for children from a prior marriage. Without it, a surviving spouse can inadvertently disinherit children by remarrying or simply spending the assets. State laws on spousal elective shares add another layer of complexity that a simple will cannot address.

Sources

- Internal Revenue Service, Estate Tax

- Internal Revenue Service, Estate and Gift Tax FAQs

- Internal Revenue Service, Estate and Gift Taxes

- Cerulli Associates, $124 Trillion Wealth Transfer Projection

- Bank of America Private Bank, 2026 Wealth Transfer and Longevity Study

- Prime Rate, What Is a 401(k) Match and How Do You Maximize It

- Prime Rate, Roth IRA vs Traditional IRA: Choosing the Right Account

- Prime Rate, How to Create a Monthly Budget That Actually Works