Fact-checked by the Prime Rate editorial team

The Verdict

A variable-rate HELOC is usually the smarter pick if prime rate is falling and your current HELOC rate is above 7.5% with no rate floor below that level. A fixed home equity loan wins if you need a lump sum, carry a tight budget, or your lender’s HELOC floor would block you from capturing any rate relief. Product structure and lender margin matter as much as Fed timing.

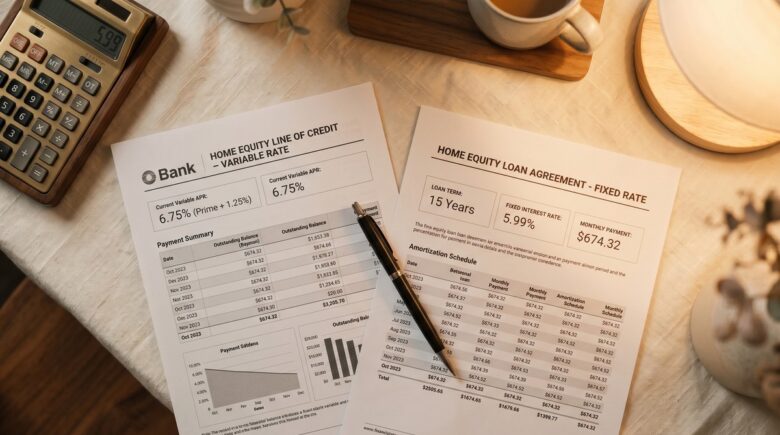

Most borrowers approach the HELOC vs home equity loan decision as a simple rate comparison, but the number that actually determines your cost is not the advertised rate, it is the margin your lender adds to the prime rate, and that number travels with you for the life of the line. As of June 3, 2026, the national average HELOC rate sits at 7.43%, while the average 5-year home equity loan runs 8.12% per Bankrate’s lender survey, a spread that looks like a clear win for HELOCs until you examine what a rate floor or a high margin does to that edge.

The Fed cut rates three times in late 2025, and at least one or two additional cuts are on the table for 2026. That makes this a genuine decision point, not a hypothetical.

| Factor | Reasons to Choose a HELOC | Reasons to Choose a Fixed Home Equity Loan |

|---|---|---|

| Rate in falling-rate environment | Adjusts down automatically within 1-2 billing cycles of a Fed cut, no refinancing required | Locked at closing; you capture zero benefit from future Fed cuts without a costly refinance |

| Current rate | National average 7.43% | National average 8.12% (5-year, $30,000) |

| Payment predictability | Variable monthly payments; a surprise rate hold or reversal raises costs immediately | Fixed payment for the loan term; nothing changes regardless of Fed action |

| Draw flexibility | Revolving line; borrow, repay, re-borrow; interest accrues only on drawn balance | Lump sum disbursed at closing; interest accrues on the full balance from day one |

| Rate floor risk | If floor is set at, say, 7.0%, you capture nothing from cuts that push prime below that level | No floor risk; your rate is already fixed and cannot rise unexpectedly |

| Ongoing fees | Annual fees of $5–$250, possible transaction fees, inactivity fees, early termination penalties of 2%–5% | Typically no annual fees; closing costs of 2%–5% are a one-time charge |

| Best use case | Phased renovations, emergency reserves, situations where flexibility has real value | Debt consolidation, one-time large expenses, fixed-income budgets where surprises are unaffordable |

Key Takeaways

- Your HELOC’s current rate is above 7.5% and your lender’s rate floor sits below that level, so you would actually capture future Fed cuts.

- Your HELOC margin is prime + 1.0% or less, rates above that benchmark mean a fixed loan may already be cheaper over a typical 5-year payoff horizon.

- You do not need the full loan amount on day one, phased draws mean you pay interest only on what you use, which a fixed lump sum cannot match.

- Your credit score is 740 or higher and your combined loan-to-value ratio is at or below 80%, unlocking the tightest HELOC margins available.

- Your monthly budget can absorb a payment increase of at least $50–$100 on a $50,000 balance if rate cuts stall or reverse, the HELOC advantage depends on the Fed delivering, not just discussing.

- You have compared offers from at least two lenders, including a credit union, since HELOC margins vary by 1.25 percentage points or more between lenders on the same balance.

- You are not using proceeds to consolidate consumer debt or fund non-home expenses where the interest deduction would not apply under IRS Publication 936.

What Are You Actually Comparing?

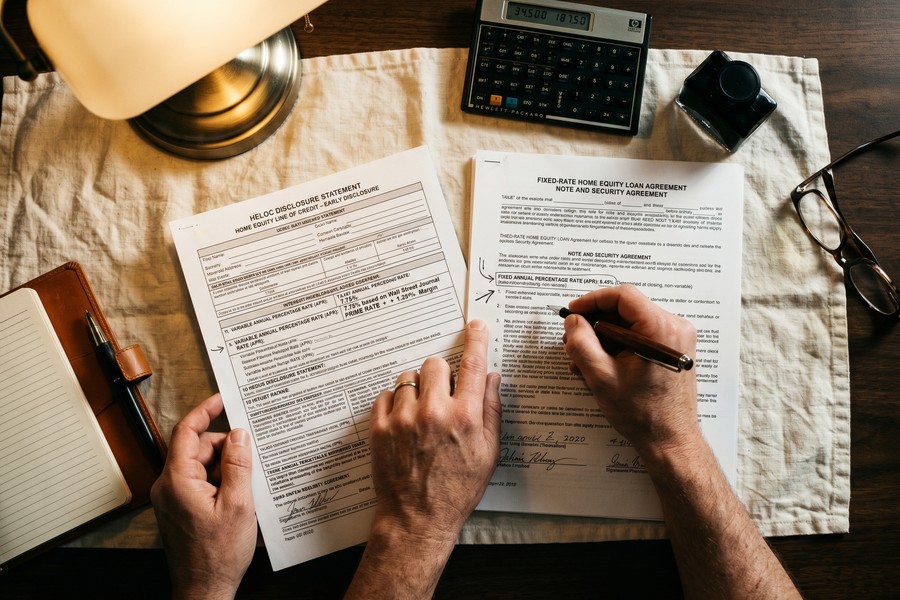

A HELOC and a home equity loan are priced off entirely different benchmarks, and that structural difference is more important than any rate forecast. A HELOC is a revolving line of credit whose rate equals a publicly available index (almost always the prime rate) plus a lender margin. Per CFPB consumer guidance, HELOCs typically carry variable rates tied directly to that index, meaning your cost of credit mirrors index changes by contract. Under Regulation Z (12 CFR § 1026.40), lenders must disclose the index, the margin, and how the APR is determined before you sign, so you have the right to those numbers in writing.

A home equity loan, by contrast, is a fixed-rate lump sum. Its rate is set at closing and tied to intermediate-term Treasury yields, not the federal funds rate. That matters because the Fed’s target rate and 10-year Treasury yields do not always move together. A fixed home equity loan rate can fall even if the Fed holds steady, or stay stubbornly high even after a Fed cut. Borrowers who delay locking in a fixed loan while waiting for a Fed announcement may already have missed the move in Treasury-driven pricing.

The number most borrowers ignore on a HELOC is the margin, not the advertised APR. The prime rate is identical across every lender; the margin is not. Lenders typically add anywhere from prime + 0.25% to prime + 2.0% or higher. On an $80,000 balance, the difference between prime + 0.25% and prime + 1.50% is roughly $1,000 per year in additional interest. That spread dwarfs the savings from one Fed cut.

Does a Falling Prime Rate Actually Favor the HELOC?

Mostly yes, but the HELOC’s edge has a concrete ceiling that most comparisons skip entirely. Existing HELOC borrowers get automatic payment relief when the Fed cuts: the prime rate adjusts within 24–48 hours of a Fed decision, and payments reset within one to two billing cycles, with no refinancing cost, no appraisal, no application. A fixed home equity loan borrower who wants that same relief must refinance the entire balance and absorb 2%–5% in new closing costs.

According to Bankrate’s analysis of Fed rate cuts and home equity, HELOC borrowers should see their rates move lower in response to any Fed rate cut, usually within one to two statement cycles, sometimes with a three-month lag.

The dollar advantage of waiting for rate cuts is real but modest at the pace currently expected. Bankrate data shows HELOCs peaked at 10.16% in early 2024 before the Fed began cutting. From that peak to today’s average of 7.43%, a borrower with a $50,000 HELOC balance has seen monthly interest drop by more than $100. But the remaining projected 2026 cuts of 0.50%–0.75% would save only about $21–$31 per month on that same balance. That is real money over a year, though not transformative.

There is also the rate floor problem, and it is bigger than most articles acknowledge. Many HELOC agreements include a floor, a minimum rate the lender will charge regardless of where prime goes. If your floor is set at 7.0% and prime falls to 6.5%, you capture zero benefit from that cut or any further cut below 7.0%. The HELOC’s entire falling-rate advantage disappears behind that floor. Check this number before you sign anything.

One more dynamic worth naming: the rate-cut benefit for new HELOC applicants is different from the benefit for existing holders. An existing holder’s rate moves down passively. A new applicant’s cost depends on what margin lenders are offering at origination, and lenders are under no obligation to pass Fed cuts through to new application pricing on the same timeline. As Jamie Slavin, Mortgage Production Manager at Ent Credit Union, noted: “They will work in tandem with the Fed funds rate at a staggered pace. The Fed makes an announcement on a rate cut, and the following month, the prime rate, which affects HELOCs, is updated for new and existing loans.”

The Fee Layer That Changes the Math

Closing costs alone do not separate these products as clearly as most borrowers expect. Both HELOCs and home equity loans typically run 2%–5% of the loan amount in closing costs, though many HELOC lenders waive or reduce upfront fees to win the origination, only to recoup margin through annual fees, transaction fees, and early termination penalties of 2%–5% of the balance. Home equity loans tend to carry a one-time closing cost with no ongoing fee structure.

The FTC’s consumer guidance on home equity products and the CFPB’s federally mandated HELOC consumer booklet both flag that lenders add a margin to the index to set the borrower’s rate, and both recommend examining how high the index has historically risen before committing to a variable-rate line. That is good advice. HELOC rates hit 10.16% just two years ago; the current 7.43% average is not the floor of the possible range.

Watch for introductory rate offers in the mid-5% to 6% range. These expire after 6–12 months, then reset to the fully indexed rate, prime plus your margin, no exceptions. Comparing a teaser HELOC rate to a fixed home equity loan rate is not a fair comparison, and some lender marketing makes this very easy to do accidentally. Ask the lender to show you the fully indexed rate at today’s prime, then compare that to the fixed loan offer.

Understanding how the prime rate affects your mortgage and home equity loan in practical terms can help you stress-test both products against multiple rate scenarios before committing.

Use Case Is the Actual Deciding Factor

The rate environment tips the scales, but the purpose of the borrowing often settles the question outright. For phased home renovations where you need capital in stages, the HELOC wins on basic math: interest accrues only on the drawn balance, not the full approved line. A contractor paid in three draws over eight months costs a HELOC borrower far less in cumulative interest than a lump-sum home equity loan disbursed at closing.

For debt consolidation on a fixed income, the fixed home equity loan is defensibly the better product regardless of rate direction. Predictable payments that will not surprise are worth more than a rate advantage that may or may not materialize. As strategic debt payoff approaches make clear, knowing exactly what you owe each month is itself a financial asset, and a HELOC’s variable payment structure strips that certainty away.

There is also a hybrid option that most comparisons bury in a footnote: the fixed-rate lock within a HELOC. Some lenders allow borrowers to convert a portion of their drawn balance into a fixed-rate sub-loan while keeping the remaining revolving line variable. This gives you rate certainty on the amount you actually need without surrendering flexible access to undrawn credit. It is worth asking any HELOC lender whether this feature is available and at what cost before assuming your only options are fully variable or fully fixed.

According to Bankrate’s reporting on home equity borrowing and Fed rate cuts, there has historically been less interest rate sensitivity on fixed-rate home equity loans when rates are falling, and borrowers seeking out home equity loans will need to shop around, since not all lenders will reduce interest rates at the same speed.

Home equity borrowing is at historically high volumes. U.S. homeowners held a record $17.8 trillion in total home equity entering Q3 2025, including $11.6 trillion in tappable equity while maintaining a 20% cushion. And according to the Mortgage Bankers Association’s 2025 Home Equity Lending Study, combined HELOC and home equity loan originations rose 7.2% in 2024. A lot of people are making this decision right now; most are doing it without a clear rate-environment framework.

Tax treatment applies equally to both products, but it trips up a large share of borrowers. Under IRS Publication 936, interest on both HELOCs and home equity loans is deductible only if the proceeds are used to buy, build, or substantially improve the home that secures the loan, a rule in place since the Tax Cuts and Jobs Act of 2017 and still in effect for 2026. Borrowers using either product to pay off credit card debt or fund a vacation cannot deduct the interest. That changes the after-tax cost calculation meaningfully, and many borrowers only discover it at tax time. If your use case is not home improvement, factor in the lost deduction when comparing net costs.

If you are managing a broader debt strategy alongside this decision, understanding how to build a monthly budget that actually works is a useful pre-step, especially if you are choosing a HELOC partly because you plan to make irregular draws rather than a single fixed payment.

Who Should and Who Should Not

Good candidates

Borrowers who have the financial flexibility to absorb variable payments and a genuine use for revolving access will get the most from a HELOC in the current environment.

- Homeowners with an existing HELOC at or above 8% who locked in before late-2025 Fed cuts, they benefit passively from every subsequent cut with no action required.

- Borrowers funding a multi-phase home renovation where draws are spread over 12–24 months and interest only accrues on what is pulled.

- Borrowers with a credit score of 740+ and combined loan-to-value at or below 80%, who can negotiate a margin of prime + 0.50% or better and meaningfully outperform a fixed loan over a falling-rate cycle.

- Anyone who wants a standing emergency credit line, open but undrawn, without paying interest on an unused lump sum.

- Borrowers who understand the rate-floor language in their agreement and have confirmed that their floor is below current prime, so they will actually capture future cuts.

Who should skip it

Certain borrower profiles are better served by the certainty of a fixed home equity loan, regardless of where rates are headed.

- Fixed-income households where a $50–$100 monthly payment increase would require cutting essential expenses, the HELOC’s variability is a liability, not a feature.

- Borrowers consolidating high-interest consumer debt who need a fixed payoff schedule to stay disciplined; revolving access makes re-borrowing too easy.

- Anyone whose HELOC agreement includes a rate floor at or above the current prime rate, the falling-rate thesis does not apply to them at all.

- Borrowers who need the full loan amount on day one and will carry that balance for five or more years; a fixed home equity loan avoids both ongoing fees and rate volatility over a long horizon.

Frequently Asked Questions

Is a HELOC better than a home equity loan when interest rates are falling?

Usually, yes, but only if your HELOC has no rate floor blocking you from capturing the cuts. Existing HELOC borrowers see their rate drop automatically within one to two billing cycles of a Fed cut, while home equity loan borrowers are locked in and would need a full refinance to get a lower rate. The margin your lender charges still matters more than Fed timing in most scenarios.

How much does a HELOC rate drop when the Fed cuts by 0.25%?

Your HELOC rate drops by exactly 0.25% once the prime rate adjusts, typically within 24–48 hours of the Fed decision, with your payment resetting one to two billing cycles later. On a $50,000 balance, that cut saves roughly $10–$11 per month, or about $125–$132 per year.

What is a HELOC rate floor and why does it matter?

A rate floor is a contractual minimum rate your lender will charge regardless of how low the prime rate falls. If your floor is 7.0% and prime drops to 6.5%, you pay 7.0%, not 6.5%, and you capture none of that Fed cut. Check your loan agreement for floor language before assuming a falling-rate environment benefits you at all.

Can I deduct HELOC interest on my taxes in 2026?

Only if you use the funds to buy, build, or substantially improve the home securing the loan. Under IRS Publication 936 and rules from the Tax Cuts and Jobs Act of 2017, interest on HELOC proceeds used for debt consolidation, a car, or any non-home purpose is not deductible. The same restriction applies to fixed home equity loans.

How do I know if a HELOC or a home equity loan is the better deal right now?

Compare the HELOC’s fully indexed rate (prime + your offered margin, not the teaser rate) to the fixed home equity loan rate after subtracting any closing cost difference. If the HELOC’s fully indexed rate is more than 0.5 percentage points below the fixed loan and your rate floor is below current prime, the HELOC likely wins over a three-to-five year horizon in a falling-rate environment. If those conditions do not hold, the fixed loan’s predictability is hard to beat. Also check whether your credit score qualifies you for the tightest margins available, since lender selection can swing your annual cost by more than any single Fed cut.

Sources

- Bankrate, Current HELOC Rates, June 2026

- Bankrate, Federal Reserve Rate Cuts and Home Equity, Greg McBride, CFA

- Consumer Financial Protection Bureau, What Is a Home Equity Line of Credit (HELOC)?

- Federal Trade Commission, Home Equity Loans and Home Equity Lines of Credit

- NRMLA / ICE Mortgage Technology, Home Equity Hits Record High, Q3 2025

- Mortgage Bankers Association, 2025 Home Equity Lending Study