Fact-checked by the Prime Rate editorial team

The Verdict

Understanding how savings account rates are set matters most if your current APY is well below the best available rate. If your bank pays 0.39% (the FDIC national average) while top online banks offer 5.00%, switching is worth the 20-minute effort. It is not worth it if branch access, bundled products, or account relationships provide genuine value that offsets the rate gap.

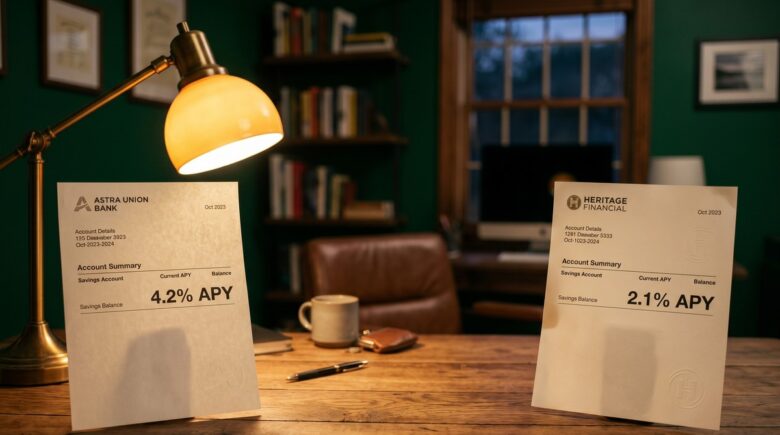

How savings account rates are set has nothing to do with a government mandate and everything to do with a bank’s cost structure, deposit needs, and competitive strategy. The single factor that swings the outcome for you is whether your bank is passing on the prevailing rate environment or quietly pocketing it. The FDIC national average APY sits at just 0.39%, while the top high-yield savings account pays 5.00% at Varo Money, a gap of more than 460 basis points on federally insured products of the same type.

That gap is not a market anomaly. It is a deliberate pricing structure, and it persists in December 2025 because most depositors never check it. After three Federal Reserve rate cuts in late 2025, savings yields are trending down from their 2023–2024 peak, which makes the window for locking in competitive rates shorter than it was a year ago.

| Factor | Reasons to Switch to a Higher-Yield Account | Reasons to Stay With Your Current Bank |

|---|---|---|

| Rate gap | Top accounts pay 5.00% APY vs. a national average of 0.39%, a $460+ annual difference on $10,000 | If your bank already pays 4%+, the switching math may not justify the effort |

| Overhead costs | Online banks spend less than 0.8% of deposits on overhead vs. ~4.5% at branch-heavy banks, funding higher yields structurally | Branch access has real value for cash deposits, notary services, or complex transactions |

| FDIC insurance | High-yield savings accounts at online banks carry the same FDIC coverage as traditional banks, up to $250,000 per depositor | If you hold multiple products (mortgage, checking, auto loan) at one bank, consolidation benefits may exist |

| Rate transparency | Online-only banks typically compound interest daily, increasing realized yield on the same nominal APY | Traditional banks may compound monthly or quarterly, fine if the advertised APY already accounts for this |

| Switching friction | Most switching tasks (relinking direct deposit, autopay) take under an hour; the interest math often recovers that time cost within weeks | If you have many linked accounts or a complex direct deposit arrangement, the setup time is real |

| Rate stability | HYSAs and CDs lock in competitive rates before further Fed cuts reduce them further in 2026 | Variable-rate accounts can drop without notice, some banks trimmed rates with no Fed action at all |

Key Takeaways

- Your current APY is at least 1.00 percentage point below the best available rate for a comparable FDIC-insured account

- You hold $5,000 or more in savings, making the annual dollar difference meaningful (every 1% gap on $10,000 is $100/year)

- You do not rely on in-branch services that your current bank provides and an online-only institution cannot replicate

- You understand that the rate you open with is variable and can change, sometimes with no Fed action as a trigger

- Your bank is a large traditional institution paying near the national average of 0.39%, not a competitive community bank or credit union

- You have verified the account has no monthly fees, minimum balance requirements, or direct deposit conditions that would erode the advertised APY

- You are willing to maintain a separate local checking account alongside an online HYSA if branch access still matters to you

What Actually Determines the Rate on Your Savings Account

No single authority sets the APY on your savings account. The rate emerges from a bank’s internal cost structure, how badly it needs new deposits, and the broader signal sent by the Federal Reserve’s benchmark rate, and none of those factors operates in lockstep with the others.

The most important distinction to understand upfront is the difference between an interest rate and an APY. The Annual Percentage Yield, as defined by the Consumer Financial Protection Bureau under Regulation DD, accounts for the effect of compounding: APY = 100 [(1 + Interest/Principal)^(365/Days in term) − 1]. Every insured institution must use this standardized formula, which is why APY is the only number worth comparing across accounts. A bank advertising a 4.80% nominal interest rate compounded monthly will produce a slightly lower realized return than a bank advertising 4.80% APY compounded daily, the headline numbers look identical, but the math differs.

Banks weigh four core variables when setting deposit rates: their overhead cost structure, current loan demand, the competitive pressure to attract deposits, and their net interest margin targets. Rate-setting is a deliberate business decision. A bank that needs deposits to fund a growing mortgage portfolio will price aggressively to attract them; a bank already flush with deposits relative to loan demand has no financial reason to pay you more. That single factor, deposit need, is the most direct explanation for why two otherwise similar institutions can sit at opposite ends of the rate spectrum on the same day.

The Federal Reserve’s Role: Influential, Not Decisive

The Fed does not set your savings rate. It sets the federal funds rate, the overnight lending rate between banks, and everything else flows from the market’s response to that signal, not from any directive.

The mechanism works like this: when the FOMC raises the federal funds rate, banks’ own borrowing costs rise, their loan revenues typically increase, and competitive pressure nudges them to pay more on deposits to attract the funding they need. When the Fed cuts, the reverse logic applies, and banks tend to move faster on the cut side. At its October 29, 2025 meeting, the FOMC cut its target range to 3-3/4 to 4 percent, the third reduction in the second half of 2025. High-yield savings account rates have been sliding since, though the gap between online banks and traditional banks remains historically wide.

The concept that explains the asymmetry is deposit beta, the proportion of a Fed rate move that a bank actually passes on to depositors. During the 2022–2023 rate-hike cycle, most large traditional banks passed on a deposit beta well below 50%, meaning they captured more than half of every rate increase in their own net interest margin rather than sharing it with savers. During rate cuts, the same banks historically move faster and more fully. This is not incidental; it is the clearest evidence that deposit rate-setting is a profit strategy, not a mechanical tracking exercise. To understand how this dynamic affects your credit card debt simultaneously, see our explainer on how the prime rate affects your credit card interest rates.

Why Two Banks Can Legally Offer Wildly Different APYs at the Same Moment

The structural answer is overhead. Traditional banks spend roughly 4.5% of deposits on branch-related costs, real estate, staff, infrastructure, while online-only banks spend less than 0.8%. That 3.7-percentage-point structural gap is not arbitrary; it is a real cost difference that branch-based institutions must recoup from somewhere, and deposit rates are one of the easiest levers to pull.

A bank’s revenue model amplifies this further. A large institution that earns most of its income from loan spreads, fee income, and wealth management can subsidize low deposit rates as a deliberate strategy, depositors are a cheap funding source precisely because most don’t shop around. A deposit-funded neobank or online HYSA provider, by contrast, competes on rate because rate is often its only differentiable product feature. The FDIC’s national rate framework defines the deposit-weighted average across all insured institutions and caps what less-than-well-capitalized banks may offer, but it places no floor on what a well-capitalized bank must pay.

Compounding frequency adds another layer that most rate comparisons ignore. Legacy core banking systems at traditional institutions often compound interest monthly or quarterly due to technical constraints. Online banks typically compound daily. On a $20,000 balance at 4.80% APY, daily versus monthly compounding produces a modest but real difference in ending balance over 12 months, a gap that compounds further over years and one that readers can verify by checking any account’s Truth in Savings disclosure, as required under CFPB Regulation DD §1030.4.

For a fuller comparison of how high-yield savings accounts stack up against other fixed-rate products in the current environment, the CD rates vs. high-yield savings comparison breaks down which vehicle makes more sense at different rate scenarios.

The Inertia Tax: How Big Banks Get Away With 0.01% APY

Low rates at large banks are not a failure of competition. They are competition working exactly as the bank intends. Brand recognition, multi-product relationships, and the genuine friction of relinking direct deposits and autopay give large institutions pricing power over their most loyal customers. The average American holds a primary savings account for roughly 17 years, according to Bankrate survey data, and inertia is a structural revenue line, not an accident.

The cost of staying put is concrete. At 0.01% APY, $10,000 earns exactly $1 in a year. At 4.00% APY, the same balance earns roughly $400. That is a $399 annual difference that requires no additional risk, both accounts carry FDIC insurance to the same $250,000 limit. Scale that to a $30,000 emergency fund and the foregone interest exceeds $1,190 per year, an amount that probably offsets most switching friction within the first billing cycle. If you are also working on building that emergency cushion from scratch, the step-by-step plan in our guide on how to build a 6-month emergency fund in 2026 is worth reading alongside this one.

What savers can control is straightforward: compare current rates against the FDIC national average, check whether the advertised APY carries conditions such as minimum balances or direct deposit requirements, and move the balance if the gap justifies it. The Fed’s rate path matters less than whether your bank is passing any of it on, according to Bankrate’s analysis of how Fed decisions flow through to deposit accounts.

The honest concession here is that branch access, in-person service, and bundled product relationships carry genuine value for some depositors. A small business owner who regularly deposits cash, a retiree who values a local banker relationship, or someone managing a complex banking relationship across checking, lending, and investment accounts may rationally accept a lower savings rate as the price of convenience. That is a legitimate trade, but it should be a conscious one, not a default.

Who Should and Who Should Not

Good candidates

Depositors who are paying an inertia tax on a meaningful balance and have not compared rates since rates started rising in 2022 stand to gain the most.

- Someone with $10,000 or more sitting at a traditional bank paying 0.01%–0.50% APY, who can open an online HYSA without disrupting their daily banking setup

- Emergency fund builders who want liquid, FDIC-insured savings working as hard as possible while they build toward a 3–6 month target

- Depositors who already use digital banking tools and have no genuine need for in-branch services, the product experience of an online HYSA will feel familiar

- Anyone who opened a high-yield account 12–18 months ago and has not checked whether the rate has stepped down from its introductory level

Who should skip it

Switching for the sake of chasing the highest published APY is not always the right call, and a few depositor profiles are better served by staying put.

- Small business owners or frequent cash depositors who rely on branch infrastructure that an online-only institution cannot replicate

- Anyone whose current bank already pays within 0.50 percentage points of the best available rate, the switching math does not justify the administrative effort at that spread

- Depositors who would keep the account balance too low to make the interest difference meaningful (under $1,000), especially if the online account carries a minimum balance requirement

- Customers who hold a mortgage, auto loan, or HELOC with their current bank and receive a documented rate discount tied to maintaining a deposit relationship

Frequently Asked Questions

Does the Federal Reserve directly set savings account interest rates?

No. The Fed sets the federal funds rate, the rate banks charge each other for overnight loans, but individual banks decide how much of that rate environment to pass on to depositors. A bank may raise or cut its savings rate before, after, or completely independent of any Fed announcement, depending on its own deposit needs and competitive position.

Why is my big bank’s savings rate so much lower than an online bank’s?

The primary reason is overhead. Traditional banks spend roughly 4.5% of deposits maintaining branches, while online-only banks spend under 0.8%, a structural gap that gives digital institutions room to pay more. Large banks also rely on customer inertia, knowing that most depositors will not switch even when the rate difference is substantial.

Is a 5% APY savings account too good to be true?

Not at FDIC-insured online banks in the current rate environment. Varo Money offered 5.00% APY as of December 25, 2025, according to Fortune’s rate tracking. The caveats to check are whether the rate is promotional, whether it requires a minimum balance or direct deposit, and how frequently interest compounds, all disclosures required under the Truth in Savings Act.

What is deposit beta and why does it matter to savers?

Deposit beta is the percentage of a Fed rate change that a bank passes on to deposit customers. A bank with a deposit beta of 30% during a rate-hike cycle keeps 70% of the increase as additional margin. Historically, big banks have passed on much less of rate hikes than they pocket from rate cuts, which is why the spread between the best and worst savings accounts widens during rising-rate environments and why checking your rate after any Fed meeting is a useful habit.

Should I use a CD instead of a high-yield savings account right now?

With the Fed cutting rates through late 2025 and further cuts possible in 2026, locking in today’s CD rates makes sense for money you will not need for 12–24 months, it protects against the rate drift that variable HYSAs are already experiencing. For emergency funds or money you may need quickly, a high-yield savings account stays the right tool because of its liquidity. The CD rates vs. high-yield savings breakdown covers the tradeoffs in detail, and the best high-yield savings accounts for 2026 lists current top rates if you want to compare options directly.

Sources

- Federal Deposit Insurance Corporation (FDIC), National Rates and Rate Caps

- Federal Reserve, FOMC Press Release, October 29, 2025

- Consumer Financial Protection Bureau, Regulation DD, Appendix A: APY Calculation Formula

- Consumer Financial Protection Bureau, Regulation DD, §1030.4: Variable Rate Disclosures

- Consumer Financial Protection Bureau, Truth in Savings Act (TISA) Examination Procedures

- Federal Reserve Bank of St. Louis (FRED), National Rate for Savings Deposits (SNDR)

- Fortune, Best Savings Account Rates, December 25, 2025 (citing Curinos and FDIC data)

- Bankrate, How the Federal Reserve Impacts Savings Account Rates (Stephen Kates, CFP)