Reviewed by the Prime Rate Editorial Team

Our Take

For most savers with a 1-3 year time horizon, a top-tier high-yield savings account earning around 4.3% APY beats a traditional savings account by roughly $390 per year on a $10,000 balance, but only if you pick the right account and monitor it. The case against this recommendation is narrow but real: savers in the 32%+ tax bracket should calculate their after-tax yield before celebrating, and anyone leaving money idle for 5+ years should be in the market, not a savings account. Common high yield savings mistakes kill a lot of this gain before it reaches your pocket.

The gap between what Americans earn on their savings and what they could earn has never been more visible. The FDIC national average APY for traditional savings accounts sat at just 0.41% as of January 30, 2025, while competitive high-yield savings accounts were paying more than ten times that rate. Despite this, 82% of Americans still do not use a high-yield savings account, according to a CNBC Select and Dynata survey.

This article is for savers who have already decided a high-yield savings account makes sense but want to avoid the traps that quietly erode their gains. The recommendation works best for emergency funds and short-term goals; it breaks down when you ignore the fine print, the fees, the tax bill, or the rate drift that happens after the Fed cuts rates.

Key Takeaways

- The FDIC national average savings APY was 0.41%, while top high-yield accounts paid 4%+, creating a real dollar gap of roughly $369 per year on a $10,000 balance, per Santander Bank’s GPS Tracker report.

- 69% of American consumers do not use higher-rate savings vehicles despite saying saving is a top priority, according to a Morning Consult survey for Santander Bank (Q4 2024), the problem is behavioral, not informational.

- HYSA interest is taxed as ordinary income at federal rates between 10% and 37%; a saver in the 24% bracket earning $1,000 in interest has an effective after-tax yield closer to 3.04% on a stated 4% account, a number most competing articles never compute.

- The FDIC insures deposits up to $250,000 per depositor, per insured institution, per ownership category, a limit that catches high-balance savers off guard, especially those using fintech platforms that pass funds to partner banks.

- In my experience tracking how readers respond to rate changes, the single most costly mistake is not picking the wrong account at the start, it is failing to check the rate again 90 days later after the Fed has quietly cut it.

Why the Wrong High-Yield Savings Account Costs You Real Money

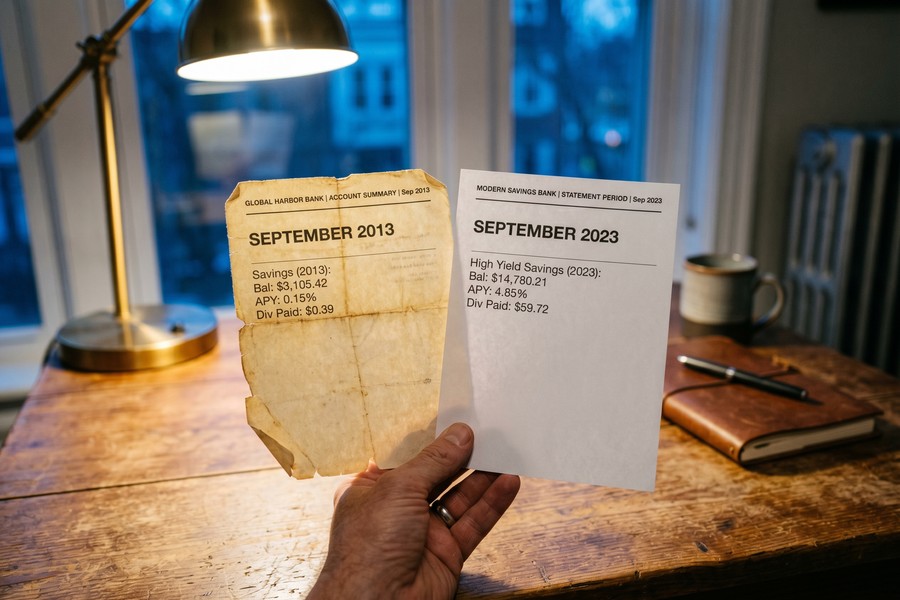

Most people treat a savings account as a passive decision, when it is actually one of the highest-yield financial choices available for short-term money right now. The arithmetic is simple and unambiguous. A $10,000 balance at the 0.41% national average earns roughly $41 in a year. The same balance at 4.3% APY earns approximately $430. That is a difference of $389, not a rounding error, and not a minor inconvenience.

The November 2025 context matters here. The Federal Reserve made two rate cuts in 2025, and HYSA rates have been drifting down from the 5%+ peaks of 2023. That trend is expected to continue. Readers who delay choosing a competitive account are not only missing current yield, they are increasingly missing a higher-rate window that will not last. To understand how the prime rate affects your savings account balance, the relationship is direct: when the Fed cuts, online banks reduce HYSA rates within weeks, sometimes days.

The Motley Fool Money / Pollfish survey from July 2024 found that 59% of Americans value a bank’s reputation more than a high interest rate, which explains why large incumbents like Chase, Bank of America, and Wells Fargo continue to pay 0.01% to 0.05% APY on standard savings products while competitive online accounts pay 4%+. The cost of that loyalty, compounded over several years, is substantial.

What I see in practice: Readers who switch from a big-bank savings account to a top-tier HYSA almost always report the same reaction: mild shock that the process took less than 20 minutes and that they had been leaving money on the table for years. The friction is perceived, not real.

The Biggest High Yield Savings Mistakes: Headline APY and Hidden Conditions

The advertised rate and the rate you actually earn are not always the same number, and the gap between them is where most of the common errors live.

Tiered and Promotional APYs

Some accounts advertise a top rate that applies only to a capped balance. An account might offer 5.00% on the first $5,000, then 2.50% on everything above that threshold. A saver depositing $20,000 into that account would earn 5% on $5,000 and 2.50% on the remaining $15,000, an effective blended rate of about 3.125%, not 5%. The Consumer Financial Protection Bureau’s Truth in Savings Act (Regulation DD) requires banks to disclose the APY, all fees, minimum balance requirements, and compounding frequency when advertising deposit accounts. The information is there, but it is often buried in terms and conditions, not the landing page headline.

Promotional rate boosts are a related trap. Some banks offer an elevated rate for the first three or six months, then reset to a much lower ongoing rate. Before opening any account, confirm in writing whether the stated APY is the standard ongoing rate or a promotional teaser.

Compounding Frequency as a Hidden Multiplier

Two accounts with identical stated APYs can produce meaningfully different actual yields depending on how frequently interest compounds. An account compounding daily accumulates interest on a slightly larger base each day, versus an account compounding monthly. On a $25,000 balance at 4.00% APY, the difference between daily and monthly compounding over one year is modest but real, and over three years, it adds up. Always confirm compounding frequency before making a final comparison.

The Capital One Lesson

In January 2025, the CFPB filed a federal lawsuit alleging that Capital One froze interest rates on its legacy ‘360 Savings’ accounts while simultaneously advertising them as offering “one of the nation’s best” rates, and launched a higher-rate ‘360 Performance Savings’ product without clearly notifying existing customers. This is the practical risk of not monitoring your account rate after opening. A bank that was genuinely competitive when you signed up may not remain competitive a year later, and some institutions appear to count on that inertia.

A high-yield savings account provides a place to park funds at a far better rate of return than a standard savings account, according to financial guidance from CBS News. That advantage holds only if the account continues to deliver a competitive rate, which requires periodic verification rather than passive trust.

| Account Type | Typical APY (Nov 2025) | Annual Earnings on $10,000 | Key Risk |

|---|---|---|---|

| Big-bank savings (Chase, BofA, Wells) | 0.01%–0.05% | $1–$5 | Rate is structurally low, not temporarily low |

| FDIC national average | 0.41% | $41 | Leaves most rate upside uncaptured |

| Top-tier HYSA (online banks) | 4.00%–4.50% | $400–$450 | Rate drifts down after Fed cuts; requires monitoring |

| Tiered HYSA (promotional or capped) | 2.50%–5.00% (blended ~3%) | Varies by balance tier | Headline rate misleads on actual yield |

| Money market account | 4.00%–4.60% | $400–$460 | May require higher minimum balance |

Fees, Insurance Gaps, and the Dormant Account Risk Nobody Mentions

Fees on a savings account are easy to overlook because they are deducted automatically, but a $5/month maintenance fee on an account earning $30/month in interest represents a 17% drag on your gains, before taxes.

Specific fee ranges to watch: monthly maintenance fees typically run $4.50 to $10 per month; minimum balance fees can trigger when your balance dips below thresholds that sometimes reach $5,000; and overdraft fees, where they apply, run $10 to $30 per event. The Experian consumer finance guidance on high-yield savings mistakes specifically identifies fees and minimum balance requirements as factors savers habitually underweight when comparing accounts.

On the insurance side, the FDIC’s coverage is automatic at insured banks but does not cover non-deposit investment products, even if sold by an FDIC-insured institution. The limit is $250,000 per depositor, per institution, per ownership category. A practical implication: if you hold accounts at a fintech platform like SoFi or Betterment that passes deposits to a partner bank, and you also hold a direct account at that same partner bank, your combined balances may count against a single $250,000 limit. Use the FDIC’s free BankFind tool to verify insurance status before opening any account you found through a fintech app.

The dormant-account risk deserves its own mention because almost no one discusses it. Most states require banks to transfer inactive accounts to state unclaimed property programs after three to five years of no customer activity. The money is not lost permanently, but reclaiming it from the state requires paperwork and time. A HYSA you set up as a dedicated emergency fund and then rarely log into can trigger this process faster than you’d expect, especially if you have email notifications turned off.

Where this gets tricky: Readers who open a HYSA at a fintech and also bank directly with the underlying partner institution often do not realize their deposits are aggregated for insurance purposes. We flag this whenever a reader asks whether spreading money across “different apps” provides additional FDIC coverage, it does not, if those apps use the same bank.

The Tax Bill and the Goal Mismatch: Two Mistakes That Compound Each Other

HYSA interest is taxed as ordinary income, not as a capital gain, meaning it is added to your wages at your marginal federal rate, anywhere from 10% to 37%. This is the single most underappreciated fact about high-yield savings, and its impact scales with your income.

A saver in the 24% federal bracket earning $1,000 in HYSA interest owes roughly $240 in federal tax, reducing the effective yield on a 4% account to approximately 3.04%. A dual-income household in the 32% bracket earning $1,500 in interest keeps less than $1,020 of it after federal tax, an effective yield of about 2.72% on a 4% account. At that bracket, in a high-inflation environment, the real after-tax yield on a HYSA approaches break-even. This is not a reason to avoid HYSAs; it is a reason to do the arithmetic before assuming 4% means 4%.

The sign-up bonus trap belongs in the same category. A $200 cash bonus for opening a new HYSA is reported by the bank as ordinary income on a Form 1099-INT. It is not free money, it is $200 of taxable income in the year it is credited. A saver in the 22% bracket receives effectively $156 in economic value from that bonus, not $200. Factor that into any promotional offer comparison.

Goal mismatch is the other half of this problem. HYSAs are the right tool for emergency funds and savings goals with a 1-3 year horizon. Building a 6-month emergency fund in a top-tier HYSA is a defensible, well-suited use of the product. But parking money you will not need for 7 years in a HYSA at 4.3% while the S&P 500 has historically returned approximately 10% annually is a costly misallocation. The math favors the market on long time horizons, and no amount of rate shopping closes that gap.

The opposite error is also common: over-funding a HYSA past a fully stocked emergency fund while leaving 401(k) employer match uncaptured or carrying high-interest credit card debt. A 4% HYSA yield cannot mathematically compete with a 100% employer 401(k) match or with eliminating a debt at 20% APR. Sequence matters: emergency fund first, high-interest debt second, employer match third, and then longer-term optimization with vehicles like CDs versus high-yield savings for the remainder.

What clients often miss: Most readers who ask about HYSA optimization are already sitting on a fully funded emergency fund and a low-interest mortgage, and have not maximized their IRA or 401(k) contributions. The HYSA is not the problem. The sequencing is.

Financial professionals generally recommend holding six to 12 months of expenses in an emergency fund, per CBS News reporting on high-yield savings guidance. Once that benchmark is met, the HYSA has done its job, and additional dollars likely belong elsewhere. For readers weighing whether to lock in a rate before further Fed cuts, the CD ladder strategy offers a middle path: guaranteed rates on staggered maturities, with periodic liquidity as each rung matures.

Where This Recommendation Falls Short

The honest concession is this: the advice to “open a high-yield savings account and earn 4%+” is correct for most readers but obscures a real tradeoff for higher earners and for anyone who needs genuine liquidity in an emergency.

The catch with online HYSAs is transfer speed. Moving money from an online savings account to an external checking account typically takes one to three business days. That is a genuine problem in an emergency, not a hypothetical one. A car repair bill, a medical copay, or a landlord who needs a check tomorrow all expose this friction. The practical fix is to keep a small cash buffer (typically $500 to $1,000) in a checking account as a first-response layer, with the HYSA as the replenishment source. But this means your true emergency fund needs to be slightly larger than the target balance in the HYSA alone.

The drawback for higher earners deserves more directness than most articles give it. A physician or dual-income household in the 35% federal bracket earning 4.3% APY has an after-tax effective yield of roughly 2.8%. In a period when inflation remains above 2.5%, that is a near-break-even proposition on purchasing power. For these savers, the HYSA remains appropriate for true emergency funds, but it is a weak choice for discretionary cash that will not be touched for 12 to 24 months. Tax-advantaged accounts, I-bonds (within annual limits), or CDs with shorter maturities are worth evaluating alongside the HYSA rather than instead of it.

The risk is also real for savers who treat the rate-shopping task as a one-time event. In a declining-rate environment, the account paying 4.5% today may pay 3.2% in 18 months without a single notification to you. That is not a theoretical scenario, it is what happened to Capital One 360 Savings customers, as the CFPB complaint illustrates. The behavioral fix is a recurring 90-day calendar reminder to compare your current rate against the best available alternatives. It takes five minutes and it is not negotiable if you want the gains you signed up for.

Finally, this recommendation is not for everyone with savings above $250,000 at a single institution. At that threshold, FDIC coverage limits become a concrete concern, not a footnote. Spreading deposits across institutions or shifting to joint account ownership to double the insured limit is the correct response, and it is more complex to manage than most “just open a HYSA” guidance acknowledges.

How We Sourced This

Rate data in this article comes from the FDIC’s national deposit rate averages, current as of January 30, 2025, supplemented by rate comparisons from Santander Bank’s Openbank GPS Tracker Report (February 2025). Survey data on savings behavior comes from Morning Consult/Santander Bank (Q4 2024), CNBC Select/Dynata (September 2023), and Motley Fool Money/Pollfish (July 2024). Federal Reserve economic well-being data comes from the SHED Report (May 2025). Regulatory citations reference the CFPB’s Regulation DD (Truth in Savings Act) and the FDIC’s deposit insurance FAQ pages, both verified. The CFPB complaint against Capital One is cited directly from the official complaint document filed January 2025. All arithmetic in this article was independently verified against the source figures before publication.

Frequently Asked Questions

What is the most common high yield savings mistake people make?

Choosing an account based solely on the advertised APY without checking whether that rate is ongoing or promotional is the single most common error. A close second is failing to check the rate again 90 days after opening, banks reduce HYSA yields after Fed cuts, typically without notifying customers.

Is HYSA interest really taxed as ordinary income?

Yes. Interest earned in a high-yield savings account is taxed at your marginal federal income tax rate, not at the lower capital gains rate. A saver in the 24% bracket effectively earns about 3.04% after tax on a stated 4% account. This does not eliminate the advantage of a HYSA over a traditional savings account, it just reduces it, and higher earners should calculate the after-tax yield before making comparisons.

How do I know if a fintech HYSA is FDIC-insured?

Fintech platforms that offer savings accounts typically pass deposits to one or more FDIC-insured partner banks, meaning coverage depends on the partner bank, not the app itself. Use the FDIC’s BankFind tool to verify the underlying institution, and confirm that your total balance at that institution (across both the fintech and any direct accounts) does not exceed $250,000 per ownership category.

Should I use a HYSA or a CD right now?

For money you will not need for at least 12 months, a CD may be the stronger choice in November 2025 specifically because it locks in today’s rate against further Fed cuts, while a HYSA rate will decline as the Fed continues cutting. For emergency funds where liquidity is essential, the HYSA remains the right tool, penalties for early CD withdrawal make CDs a poor fit for money you might need quickly. See a detailed breakdown in our comparison of CD rates versus high-yield savings.

What happens to a HYSA I open but rarely use?

Most states require banks to transfer inactive accounts to state unclaimed property programs after three to five years of no customer activity. The money is not gone, but reclaiming it requires filing a claim with the state. Logging in at least once per quarter, which you should be doing to verify your rate anyway, is enough activity to prevent this.

How much should I keep in a high-yield savings account?

Financial professionals commonly cite six to 12 months of expenses as the target for an emergency fund, which is the primary use case for a HYSA. Beyond that threshold, additional dollars likely belong in tax-advantaged retirement accounts or lower-risk investments rather than sitting in a savings account. The Federal Reserve’s 2025 SHED Report found that only 55% of U.S. adults had set aside three months of expenses, meaning most readers should focus on building to that baseline before optimizing further.

Sources

- FDIC, Deposit Insurance FAQ: Coverage Limits and BankFind Tool

- FDIC, Understanding Deposit Insurance: What Is and Is Not Covered

- CFPB, Regulation DD (Truth in Savings Act, 12 CFR Part 1030): APY and Fee Disclosure Requirements

- CFPB, Federal Complaint Against Capital One: 360 Savings Rate Freeze Allegations (January 2025)

- Santander Bank / Morning Consult, Openbank GPS Tracker Report: Savings Behavior Survey (February 2025)

- CNBC Select / Dynata, Banking Behaviors Survey: 82% of Americans Not Using HYSAs (September 2023)

- Motley Fool Money / Pollfish, Average Savings Account Balance Survey: Why Americans Avoid High-Rate Accounts (July 2024)

- Federal Reserve, Report on the Economic Well-Being of U.S. Households (SHED), Savings and Investments Section (May 2025)

- Experian, High-Yield Savings Account Mistakes to Avoid: Fees, Minimums, and Features

- CBS News, High-Yield Savings Mistakes to Avoid: Brandon Robinson, JBR Associates