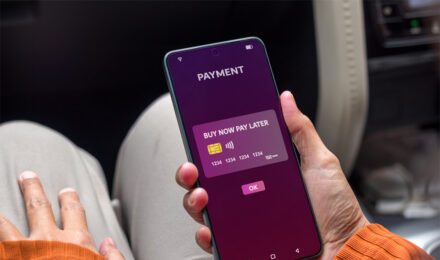

Buy Now, Pay Later services have exploded in popularity. Apps like Affirm, Klarna, and Afterpay promise a simple deal: split your purchase into smaller chunks, often interest-free. For millions of millennials, this feels like a financial superpower. But beneath the sleek interfaces and “zero interest” promises, a more complex story unfolds. BNPL can be a smart budgeting tool — or a fast track to financial trouble. Understanding which side you land on requires a closer look at the hidden costs, the psychological shifts, and the regulatory landscape shaping this fintech phenomenon.

The Hidden Cost of Splitting Your Payments

The “Free Money” Illusion

BNPL providers market themselves as the antidote to credit card debt. No interest. No hard credit checks. Just four easy payments. It sounds almost too good to be true — and sometimes it is. While many BNPL plans genuinely charge zero interest, the real costs hide in the fine print.

Miss a payment, and late fees kick in fast. Afterpay, for instance, charges up to $8 per missed installment. Klarna can send delinquent accounts to collections agencies. These penalties may seem small individually. But they compound quickly when you juggle multiple BNPL plans simultaneously.

According to a 2023 report from the Consumer Financial Protection Bureau, the average BNPL user carries multiple active loans at once. That fragmentation makes tracking due dates harder. It also increases the likelihood of missed payments and cascading fees.

The Credit Score Blind Spot

Here’s a cost many consumers overlook: BNPL’s complicated relationship with credit reporting. Historically, most BNPL providers didn’t report payment activity to credit bureaus. That meant on-time payments did nothing to build your credit score. Missed payments, however, could still damage it once accounts went to collections.

This dynamic is shifting. Companies like Affirm now report to Experian and TransUnion. But the reporting remains inconsistent across the industry. You can’t assume your responsible BNPL behavior helps your credit profile.

For millennials working to build or repair credit, this inconsistency creates a blind spot. You might think you’re managing debt responsibly. Meanwhile, your credit report tells a different story — or no story at all.

The Opportunity Cost You Don’t See

Every BNPL installment represents money committed to a past purchase. That’s money you can’t direct toward savings, investments, or an emergency fund. Financial planners call this “opportunity cost.” It rarely shows up in BNPL marketing.

Consider a practical example. You split a $200 purchase into four $50 payments. Each payday, $50 disappears before you even think about saving. Multiply that across three or four active BNPL plans. Suddenly, $150–$200 of each paycheck goes toward past spending.

NerdWallet’s 2024 analysis found that 42% of BNPL users have made a late payment. Many cited overextension as the primary reason. The convenience of splitting payments masked how much future income they’d already committed.

How BNPL Reshapes Your Financial Habits

The Psychology of Painless Spending

BNPL changes how your brain processes purchases. Traditional payment methods create “pain of paying.” You feel the sting when cash leaves your wallet or your bank balance drops. BNPL dulls that pain. It breaks one uncomfortable transaction into several smaller, barely noticeable ones.

Behavioral economists have studied this effect extensively. Smaller payments feel more manageable. They reduce the psychological friction that normally prevents impulse purchases. You buy more because each individual payment feels insignificant.

A 2023 study cited by BBC News found that BNPL users spend 20–30% more per transaction than those paying upfront. That’s not a budgeting tool. That’s a spending accelerator disguised as financial flexibility.

Normalizing Debt for Everyday Purchases

BNPL used to target big-ticket items. Furniture. Electronics. Medical bills. Now it’s everywhere. You can split a $30 meal delivery or a $15 subscription box into installments. This normalization of micro-debt represents a fundamental shift in consumer behavior.

Millennials grew up watching their parents navigate the 2008 financial crisis. Many developed a healthy skepticism toward credit cards. BNPL bypasses that skepticism. It doesn’t feel like debt because no one calls it debt.

But functionally, it is debt. You owe money for something you’ve already consumed. Reframing that obligation as “installments” or “payment plans” doesn’t change the underlying financial reality. It just makes it easier to ignore.

Where Regulation Is Heading

The regulatory environment around BNPL is evolving rapidly. The CFPB issued an interpretive rule in 2024 classifying BNPL providers as credit card lenders. This subjects them to similar disclosure requirements and consumer protections.

This means BNPL companies must now provide billing statements. They must investigate disputes. They must issue refunds more transparently. These changes benefit consumers significantly.

Several states are also introducing their own oversight measures. For millennials, staying informed about these regulatory shifts matters. The BNPL product you use today may operate under very different rules tomorrow. Understanding your protections helps you make smarter choices.

Making BNPL Work for You

BNPL isn’t inherently bad. It becomes problematic when users treat it as free money rather than a budgeting commitment. Here’s how to use it responsibly:

- Limit active plans. Never carry more than one or two BNPL obligations simultaneously. Track each due date in your calendar or budgeting app.

- Reserve BNPL for planned purchases. If you wouldn’t buy it with cash today, splitting the payment doesn’t make it more affordable. It just delays the financial impact.

Treat every BNPL installment like a bill. Budget for it before you commit. If adding another payment plan strains your monthly cash flow, that’s a clear signal to walk away from the purchase.

Buy Now, Pay Later occupies a complicated space in personal finance. It offers genuine flexibility for disciplined users. It also creates real risks for anyone who confuses convenience with affordability. The key distinction lies in intentionality. Use BNPL as a planned budgeting tool, and it can serve you well. Use it to avoid the discomfort of spending money you don’t have, and it quietly erodes your financial health. As regulations tighten and credit reporting catches up, the stakes of misusing BNPL will only grow. The smartest move? Treat every “pay later” commitment with the same seriousness you’d give any other debt — because that’s exactly what it is.

References

- Consumer Financial Protection Bureau. “Buy Now, Pay Later: Market Trends and Consumer Impacts.” https://www.consumerfinance.gov/data-research/research-reports/buy-now-pay-later-market-trends-and-consumer-impacts/

- NerdWallet. “Buy Now, Pay Later Statistics.” https://www.nerdwallet.com/article/finance/buy-now-pay-later-statistics

- BBC News. “Buy Now Pay Later: The Risks Behind the Convenience.” https://www.bbc.com/news/business-buy-now-pay-later

Buy Now, Pay Later services have exploded in popularity. Apps like Affirm, Klarna, and Afterpay promise a simple deal: split your purchase into smaller chunks, often interest-free. For millions of millennials, this feels like a financial superpower. But beneath the sleek interfaces and “zero interest” promises, a more complex story unfolds. BNPL can be a smart budgeting tool — or a fast track to financial trouble. Understanding which side you land on requires a closer look at the hidden costs, the psychological shifts, and the regulatory landscape shaping this fintech phenomenon.

The Hidden Cost of Splitting Your Payments

The “Free Money” Illusion

BNPL providers market themselves as the antidote to credit card debt. No interest. No hard credit checks. Just four easy payments. It sounds almost too good to be true — and sometimes it is. While many BNPL plans genuinely charge zero interest, the real costs hide in the fine print.

Miss a payment, and late fees kick in fast. Afterpay, for instance, charges up to $8 per missed installment. Klarna can send delinquent accounts to collections agencies. These penalties may seem small individually. But they compound quickly when you juggle multiple BNPL plans simultaneously.

According to a 2023 report from the Consumer Financial Protection Bureau, the average BNPL user carries multiple active loans at once. That fragmentation makes tracking due dates harder. It also increases the likelihood of missed payments and cascading fees.

The Credit Score Blind Spot

Here’s a cost many consumers overlook: BNPL’s complicated relationship with credit reporting. Historically, most BNPL providers didn’t report payment activity to credit bureaus. That meant on-time payments did nothing to build your credit score. Missed payments, however, could still damage it once accounts went to collections.

This dynamic is shifting. Companies like Affirm now report to Experian and TransUnion. But the reporting remains inconsistent across the industry. You can’t assume your responsible BNPL behavior helps your credit profile.

For millennials working to build or repair credit, this inconsistency creates a blind spot. You might think you’re managing debt responsibly. Meanwhile, your credit report tells a different story — or no story at all.

The Opportunity Cost You Don’t See

Every BNPL installment represents money committed to a past purchase. That’s money you can’t direct toward savings, investments, or an emergency fund. Financial planners call this “opportunity cost.” It rarely shows up in BNPL marketing.

Consider a practical example. You split a $200 purchase into four $50 payments. Each payday, $50 disappears before you even think about saving. Multiply that across three or four active BNPL plans. Suddenly, $150–$200 of each paycheck goes toward past spending.

NerdWallet’s 2024 analysis found that 42% of BNPL users have made a late payment. Many cited overextension as the primary reason. The convenience of splitting payments masked how much future income they’d already committed.

How BNPL Reshapes Your Financial Habits

The Psychology of Painless Spending

BNPL changes how your brain processes purchases. Traditional payment methods create “pain of paying.” You feel the sting when cash leaves your wallet or your bank balance drops. BNPL dulls that pain. It breaks one uncomfortable transaction into several smaller, barely noticeable ones.

Behavioral economists have studied this effect extensively. Smaller payments feel more manageable. They reduce the psychological friction that normally prevents impulse purchases. You buy more because each individual payment feels insignificant.

A 2023 study cited by BBC News found that BNPL users spend 20–30% more per transaction than those paying upfront. That’s not a budgeting tool. That’s a spending accelerator disguised as financial flexibility.

Normalizing Debt for Everyday Purchases

BNPL used to target big-ticket items. Furniture. Electronics. Medical bills. Now it’s everywhere. You can split a $30 meal delivery or a $15 subscription box into installments. This normalization of micro-debt represents a fundamental shift in consumer behavior.

Millennials grew up watching their parents navigate the 2008 financial crisis. Many developed a healthy skepticism toward credit cards. BNPL bypasses that skepticism. It doesn’t feel like debt because no one calls it debt.

But functionally, it is debt. You owe money for something you’ve already consumed. Reframing that obligation as “installments” or “payment plans” doesn’t change the underlying financial reality. It just makes it easier to ignore.

Where Regulation Is Heading

The regulatory environment around BNPL is evolving rapidly. The CFPB issued an interpretive rule in 2024 classifying BNPL providers as credit card lenders. This subjects them to similar disclosure requirements and consumer protections.

This means BNPL companies must now provide billing statements. They must investigate disputes. They must issue refunds more transparently. These changes benefit consumers significantly.

Several states are also introducing their own oversight measures. For millennials, staying informed about these regulatory shifts matters. The BNPL product you use today may operate under very different rules tomorrow. Understanding your protections helps you make smarter choices.

Making BNPL Work for You

BNPL isn’t inherently bad. It becomes problematic when users treat it as free money rather than a budgeting commitment. Here’s how to use it responsibly:

- Limit active plans. Never carry more than one or two BNPL obligations simultaneously. Track each due date in your calendar or budgeting app.

- Reserve BNPL for planned purchases. If you wouldn’t buy it with cash today, splitting the payment doesn’t make it more affordable. It just delays the financial impact.

Treat every BNPL installment like a bill. Budget for it before you commit. If adding another payment plan strains your monthly cash flow, that’s a clear signal to walk away from the purchase.

Buy Now, Pay Later occupies a complicated space in personal finance. It offers genuine flexibility for disciplined users. It also creates real risks for anyone who confuses convenience with affordability. The key distinction lies in intentionality. Use BNPL as a planned budgeting tool, and it can serve you well. Use it to avoid the discomfort of spending money you don’t have, and it quietly erodes your financial health. As regulations tighten and credit reporting catches up, the stakes of misusing BNPL will only grow. The smartest move? Treat every “pay later” commitment with the same seriousness you’d give any other debt — because that’s exactly what it is.

References

- Consumer Financial Protection Bureau. “Buy Now, Pay Later: Market Trends and Consumer Impacts.” https://www.consumerfinance.gov/data-research/research-reports/buy-now-pay-later-market-trends-and-consumer-impacts/

- NerdWallet. “Buy Now, Pay Later Statistics.” https://www.nerdwallet.com/article/finance/buy-now-pay-later-statistics

- BBC News. “Buy Now Pay Later: The Risks Behind the Convenience.” https://www.bbc.com/news/business-buy-now-pay-later

: Passing null to parameter #1 ($string) of type string is deprecated in <b>/var/www/primerate.com/public/wp-content/themes/modo/single.php</b> on line <b>128</b><br />

' ,'https://primerate.com/wp-content/uploads/2026/02/Buy-Now-Pay-Later.jpg')){kind=link}