Quick Answer

A 0.5% increase in the prime rate adds $125 annually to interest on a $25,000 personal line of credit in Illinois. This assumes a typical margin of 4% above prime, resulting in a $10.42 monthly increase. Illinois lenders must provide 30-day notice of rate changes, and state usury laws cap unsecured loan APRs at 18%.

Updated July 2026

This article is part of the How Prime Rate Changes Impact Your Variable-Rate Debt Payments guide. It focuses on the specific financial effect of a 0.5% prime rate increase on a $25,000 personal line of credit in Illinois. Understanding this impact helps borrowers anticipate budget shifts and act before payments rise.

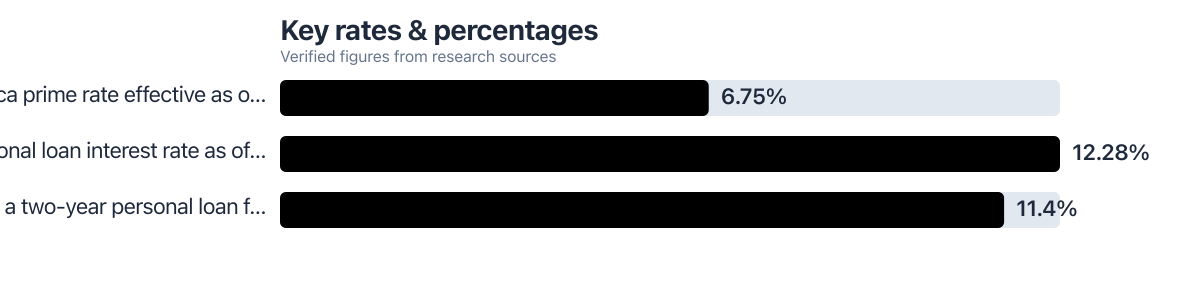

, the Federal Reserve has maintained the federal funds rate at 3.63%. This keeps the prime rate steady at 6.75%, a level confirmed by Bank of America as of December 11, 2025 [Bank of America, 2025]. This rate, set by major banks, serves as the benchmark for variable-rate loans nationwide. In Illinois, personal lines of credit tied to the Wall Street Journal prime rate will reflect any changes. This article breaks down the exact cost increase, state-specific protections, and actionable steps for borrowers.

Key Takeaways

- A 0.5% prime rate hike increases annual interest on a $25,000 personal LOC by $125 at a 4% margin, per Federal Reserve data on variable loan pricing [NerdWallet, 2026].

- Illinois law requires lenders to provide 30 days’ notice before raising variable rates on personal lines of credit, a consumer protection not found in all states.

- Illinois unsecured personal LOCs are capped at an 18% APR by state usury laws, which can limit the full impact of a prime rate increase.

- For borrowers with a 700+ FICO score, the margin above prime is typically 4% to 8%, meaning a 0.5% rate hike adds $10.42 per month on a $25,000 balance.

What happens if the prime rate goes up by 0.5%?

The prime rate is currently 6.75%, as posted by Bank of America [Bank of America, 2025]. A 0.5% rise would push it to 7.25%.

Most unsecured personal lines of credit in Illinois add a margin to the prime rate. This margin depends on creditworthiness. Borrowers with good credit typically get a margin of 4% to 8% above prime.

With a 4% margin, a $25,000 balance has an APR of 10.75% before the hike. After the increase, the APR becomes 11.25%.

How do variable-rate personal lines adjust to rate changes?

When the prime rate rises, variable-rate lines adjust in the next billing cycle. The change isn’t immediate. It appears on the next statement after the rate adjustment.

Lenders use the prime rate as a base. They add a borrower-specific margin. For example, a borrower with a 700 FICO score may have a margin of 4% to 8%. That margin stays fixed unless the credit profile changes.

For a $25,000 balance, a 0.5% prime rise adds $125 per year in interest. This is consistent with Federal Reserve data on consumer installment loan pricing [NerdWallet, 2026]. The increase is not compounded monthly unless the balance carries over.

Illinois credit unions, which offer most personal LOCs in the state, are required to follow WSJ prime and publish a maximum APR of 18%. This provides a hard limit on how much rates can rise.

How much will a 0.5% prime rate hike cost me?

A 0.5% increase in the prime rate adds exactly $125 in annual interest on a $25,000 balance, assuming a 4% margin above prime.

Breakdown: $25,000 × 0.5% = $125 per year. Divided by 12 months, that’s $10.42 per month.

This assumes the full balance is drawn and no payments are made. If the borrower makes interest-only payments, the increase is immediate. If payments reduce the balance, the impact is smaller.

How do Illinois laws affect this rate increase?

Illinois has strict usury laws. Unsecured personal loans and LOCs cannot exceed an 18% APR. This caps the maximum rate lenders can charge.

If a prime rate rise pushes a borrower’s APR above 18%, the lender must cap it at 18%. This protects borrowers from excessive rate hikes.

Lenders must also provide 30 days’ written notice before changing rates on variable products. This gives borrowers time to plan. For example, a borrower can pay down the balance before the new rate takes effect.

| Margin Above Prime | APR Before Hike | APR After Hike | Monthly Increase |

|---|---|---|---|

| 4% | 10.75% | 11.25% | $10.42 |

| 8% | 14.75% | 15.25% | $20.83 |

| 14% | 20.75% | 21.25% | $36.46 |

How does credit score affect your margin?

Borrowers with a 700+ FICO score typically get a margin of 4% to 8% above prime. Those with a 600–699 score see margins of 8% to 14%.

For a $25,000 LOC, a 0.5% prime increase adds $10.42 monthly at a 4% margin. At an 8% margin, the increase is $20.83 per month.

Illinois credit unions set rates based on credit score tiers. A borrower with a 620 FICO may pay 12.28% APR, well below the 18% cap. This reduces risk from rate hikes.

Note: Borrowers with poor credit (FICO below 600) may face margins over 14%. For them, a 0.5% prime increase could add nearly $37 monthly. This makes refinancing especially urgent, but not possible for everyone. Those with low credit scores may not qualify for new loans, even at fixed rates.

What can you do to avoid higher payments?

Refinancing to a fixed-rate personal loan is the most effective option. For example, a 3-year loan with a 700 FICO score had an average rate of 12.28%, according to Bankrate’s 2026 data.

Another option is a balance transfer to a 0% intro APR credit card. Some cards offer 18 months of 0% interest, allowing time to pay down the balance.

Consider How to Automate Savings and Debt Payments on Irregular Income if your income fluctuates. Setting up automatic payments helps avoid missed deadlines and keeps balances low.

Related reading: personal line credit rate lock.

Frequently Asked Questions

How much more will I pay monthly with a 0.5% prime increase?

If your margin is 4%, you’ll pay $10.42 more per month on a $25,000 balance. This is based on a $125 annual increase divided by 12 months.

Does Illinois use usury laws for personal lines of credit?

Yes. Illinois caps the APR on unsecured personal lines of credit at 18%. Even if the prime rate rises, your rate cannot exceed this limit.

How far in advance do I need to know of a rate change?

Lenders must provide 30 days’ written notice before raising the rate on a variable-rate personal LOC. This allows time to prepare or adjust payments.

Can I refinance if my rate increases?

Yes. You can refinance to a fixed-rate personal loan. Average rates for a 3-year loan are 12.28% for a 700 FICO score, per Bankrate (2026). This locks in a stable rate.