Quick Answer

To pay off debt fast, choose the Avalanche method (highest interest first) to save the most money, or the Snowball method (smallest balance first) if you need motivational wins. The right pick depends on your psychology and balance mix. The average credit card APR sits at 20.78%, making method selection more financially consequential than ever.

Knowing how to pay off debt fast is not simply about working harder, it is about choosing the right sequencing strategy for your specific debt profile. According to Federal Reserve G.19 consumer credit data, Americans carry more than $1.37 trillion in revolving credit card debt as of early 2025, and the sequencing of repayment directly determines how much interest you surrender.

This guide takes a decisional, psychology-informed approach, cutting through the theory to help you match the right method to your actual behavior, income pattern, and debt mix. You will leave knowing which strategy wins mathematically, which wins behaviorally, and when to combine both.

Key Takeaways

- The Avalanche method saves more money in nearly every scenario, on a $15,000 debt load at mixed rates, it can save $1,200–$2,000 in interest compared to Snowball (Consumer Financial Protection Bureau debt repayment tool).

- The Snowball method produces faster early wins, research published in the Harvard Business Review found that focusing on the smallest balance increases the probability of becoming debt-free.

- The average U.S. household carrying credit card debt pays roughly $1,380 per year in interest charges alone, according to NerdWallet’s 2025 credit card rate analysis.

- 22% of Americans report having no plan for paying down debt, meaning method selection is itself a significant competitive advantage (Federal Reserve Survey of Consumer Finances).

- A hybrid “Snowlanche” strategy, eliminating one small balance first for momentum, then switching to Avalanche, is validated by behavioral finance studies and is often the optimal real-world approach.

In This Guide

- Which Method Actually Saves You More Money?

- Does Your Psychology Determine Which Method Works?

- How Does the Snowball Method Work in Practice?

- How Does the Avalanche Method Work in Practice?

- When Should You Combine Both Methods?

- What Else Can Speed Up Debt Payoff Beyond the Method?

- Frequently Asked Questions

Which Method Actually Saves You More Money?

Targeting your highest-interest debt first, the Avalanche method, saves more money in virtually every mathematical scenario. By hitting the most expensive rate before anything else, you reduce the principal that compounds at that rate, which cuts total interest paid across the entire repayment timeline.

Consider a realistic example: $15,000 spread across three accounts, a $6,000 credit card at 24% APR, a $5,000 store card at 19% APR, and a $4,000 personal loan at 12% APR. Paying minimums plus $300 extra each month, the Avalanche method clears the debt in approximately 38 months with roughly $3,900 in total interest. The Snowball method targeting the $4,000 loan first takes approximately 40 months and costs close to $5,100 in interest, a difference of more than $1,200.

The Interest Rate Gap Matters

The larger the spread between your highest and lowest APR, the more interest-rate sequencing outperforms. If all your debts carry similar rates, say 18% to 20%, the mathematical advantage narrows and the psychological benefits of Snowball become relatively more important.

At today’s average credit card APR of 20.78%, according to Bankrate’s current credit card rate tracker, the gap between typical consumer debts is wide enough that Avalanche provides a meaningful edge for most households.

| Method | Target Debt First | Avg. Months to Payoff* | Estimated Total Interest* | Best For |

|---|---|---|---|---|

| Avalanche | Highest APR balance | 38 | $3,900 | Minimizing total cost |

| Snowball | Smallest balance | 40 | $5,100 | Building momentum fast |

| Snowlanche (Hybrid) | One small debt, then highest APR | 39 | $4,200 | Motivation + savings balance |

*Based on $15,000 total debt across three accounts at mixed rates of 12–24% APR, with $300/month above minimums.

American households carrying credit card debt pay an average of $1,380 per year in interest, nearly $115 per month that builds no equity and delivers no asset. Choosing a structured payoff method from day one eliminates that cost faster than any budgeting tweak alone.

Does Your Psychology Determine Which Method Works?

Your behavioral profile matters as much as the math. The best repayment strategy is the one you will stick with for 24, 36, or 48 months. A mathematically superior plan abandoned after six months costs far more than a slightly less optimal plan executed consistently.

A landmark study published in the Harvard Business Review by researchers Remi Trudel and David Gal found that consumers who concentrated payments on the smallest account were significantly more likely to eliminate all their debt than those who spread payments proportionally. The act of closing an account entirely creates a psychological “completion effect” that fuels continued behavior.

Identifying Your Repayment Personality

If you have ever abandoned a diet, gym routine, or savings plan within two months, the Snowball method may keep you engaged through quick wins. If you are analytically motivated, someone who can sustain effort knowing the eventual payoff is larger, Avalanche suits you better.

Research from the Association for Psychological Science reinforces this: closing individual accounts activates goal-completion reward circuits in ways that reducing a large balance does not, even when the large-balance reduction is objectively greater.

Behavioral economists call the satisfaction of eliminating a debt account entirely the “zero-balance effect.” It is the same cognitive mechanism that makes people feel better after finishing a small task list than after partially completing a complex one, and it is a legitimate reason to choose Snowball over pure math optimization.

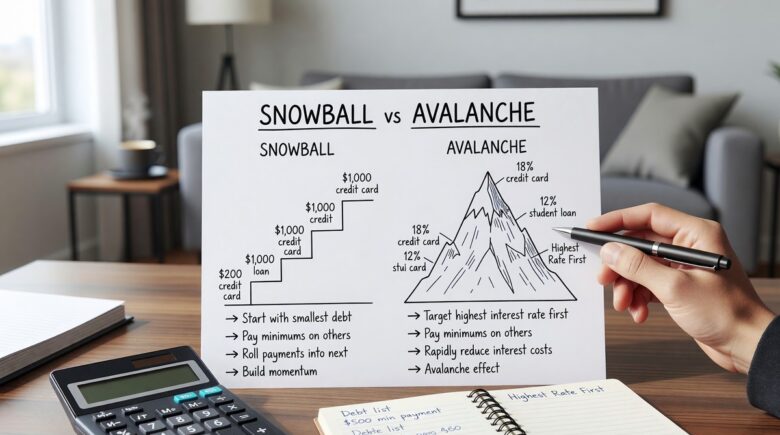

How Does the Snowball Method Work in Practice?

The Snowball method is straightforward: list all debts by balance from smallest to largest, pay minimums on all, and throw every extra dollar at the smallest balance. Once that account reaches zero, redirect its entire payment to the next smallest. The payment “snowballs” in size as each debt closes.

The mechanics are deliberately simple. Dave Ramsey, the founder of Ramsey Solutions, popularized this approach through his Financial Peace University program, which has reached over 10 million households since its launch. Ramsey’s framework deliberately ignores interest rates in favor of behavior change, an approach validated for audiences who need emotional reinforcement over mathematical precision.

Snowball in a Real Household Scenario

Suppose you have four debts: a $800 medical bill, a $2,200 store card, a $5,500 auto loan, and a $9,000 credit card. Under Snowball, you attack the $800 medical bill first regardless of its interest rate. Eliminating it in two to three months frees that payment to accelerate the $2,200 store card, and so on.

The sequence closes four distinct psychological loops rather than chipping away at one large balance indefinitely, which is why completion rates for Snowball practitioners tend to be higher among people who struggle with debt payoff burnout.

That said, Snowball is a poor fit if your smallest debt also carries the lowest interest rate by a wide margin. In that case, you pay the most for your psychological boost. Borrowers with a high-rate, small-balance debt and a low-rate, large-balance debt effectively get Snowball and Avalanche for free simultaneously, but that alignment is rarer than most guides acknowledge.

How Does the Avalanche Method Work in Practice?

Pay minimums on everything else, then direct every surplus dollar to the account with the highest APR until it is gone. Then move to the next highest rate. That is the entire framework, and the math behind it is sound.

This is the method endorsed by most financial institutions and credit counseling organizations. The National Foundation for Credit Counseling (NFCC) recommends interest-rate targeting as the baseline framework for clients who can maintain discipline through longer initial payoff cycles.

When Avalanche Takes Longer to Feel Like Progress

The Avalanche method’s biggest practical challenge is patience. If your highest-APR debt also has the largest balance, a $12,000 credit card at 27% APR, for instance, you may spend 18 months attacking it before you close a single account. That psychological void is where many Avalanche attempts stall.

To counter this, financial planners often recommend tracking interest saved rather than tracking balances. Seeing that you have avoided $220 in interest charges this month provides a data-driven win that substitutes for the emotional win of a zero balance. You might also consider learning how to negotiate lower interest rates on your credit cards, even a 2–3 percentage point reduction on your Avalanche target debt meaningfully compresses your timeline.

Avalanche also demands that your income be stable enough to sustain a fixed monthly surplus over a long stretch. Freelancers, commission earners, and gig workers often find this difficult. A single missed month on a large, high-rate balance can undo several months of progress, particularly early in the repayment window when the principal has barely moved. That is not a reason to avoid the method, it is a reason to pair it with a cash buffer before starting.

When Should You Combine Both Methods?

The Snowlanche strategy, a hybrid that eliminates one or two small debts first for momentum, then shifts to Avalanche sequencing, is the most practical approach for borrowers with mixed debt profiles. It trades a small amount of mathematical efficiency for a meaningful improvement in behavioral follow-through.

The approach works best when you have one balance under $1,000 that could be cleared in 60 to 90 days. Eliminating it quickly costs minimal extra interest, but the payoff resets your confidence and reinforces the habit of directing surplus cash to debt rather than discretionary spending.

How to Implement the Snowlanche

- List all debts by balance and by APR side by side.

- Identify any balance you can realistically eliminate within 90 days.

- Clear that one account first, paying minimums on all others.

- Once that account closes, immediately switch to Avalanche, highest APR next, regardless of balance.

- Maintain the freed payment from the closed account as part of your surplus.

If cash flow is inconsistent, a common issue for gig workers, freelancers, or commission earners, the guide on handling a financial setback without resetting your entire plan offers a complementary framework for staying on track when income fluctuates.

The term “Snowlanche” was coined by personal finance educators to describe the hybrid approach that emerged from behavioral finance research. While neither Ramsey Solutions nor the NFCC formally endorses it by name, certified financial planners increasingly recommend it as the most adherence-friendly method for clients with three or more distinct debts.

What Else Can Speed Up Debt Payoff Beyond the Method?

Method selection is foundational, but several acceleration levers can compound your results regardless of whether you choose Snowball, Avalanche, or Snowlanche. The most impactful is increasing your monthly surplus, either by cutting expenses or adding income, since even $100 extra per month can shorten a 48-month payoff timeline by six to eight months.

According to the CFPB’s debt repayment calculator, adding $200 to monthly payments on a $10,000 balance at 21% APR reduces total interest paid by more than $2,400 and cuts payoff time by nearly two years.

Debt Consolidation as a Rate Reducer

If your credit score qualifies you, a debt consolidation loan can lower your blended interest rate dramatically, sometimes from 22% to 10% or below, which makes any repayment method work faster. This is not a method replacement; it is a rate optimization that amplifies whichever sequencing strategy you apply.

A balance transfer to a 0% introductory APR credit card can effectively freeze interest on one account for 12 to 21 months, allowing your full surplus payment to attack principal. Current options are covered in our roundup of the best credit cards for 2026.

The Credit Score Feedback Loop

Paying down debt, especially revolving credit card balances, directly improves your credit utilization ratio, which is the second most heavily weighted factor in your FICO Score, accounting for roughly 30% of the total. Lower utilization can lift your score within 30 to 60 days of a balance drop, potentially qualifying you for better refinancing rates mid-repayment.

Our guide on how to build credit fast in 2026 covers the specific levers that move the number quickly. Avoiding new debt products during your payoff window is equally important, Buy Now, Pay Later services in particular can quietly fragment your debt picture and undermine sequencing discipline.

Set up a separate high-yield savings account as a debt acceleration buffer. Direct any windfall income, tax refunds, bonuses, side-hustle revenue, into this account, then deploy it as a lump-sum payment on your current Avalanche or Snowball target at the end of each month. This preserves liquidity mid-month while maximizing principal reduction. Current high-yield savings rates above 4% mean your buffer also earns while it waits.

Frequently Asked Questions

What is the fastest way to pay off debt?

Maximize your monthly surplus, apply it using the Avalanche method (highest APR first), and reduce your interest rate through consolidation or balance transfers where possible. Combining all three tactics can cut a standard 48-month payoff to under 30 months for many borrowers.

Is the Snowball or Avalanche method better for someone with credit card debt specifically?

For credit card debt, Avalanche is usually the better choice because rates are high, averaging 20.78% in 2025, and the interest savings from targeting the most expensive card first are substantial. If you have several cards with similar rates and different balances, Snowball’s quick wins may keep you more engaged without costing much extra interest.

How long does it realistically take to pay off $10,000 in debt?

At $10,000 in credit card debt with a 21% APR and $400 per month in payments, payoff takes approximately 32 months using the Avalanche method, with about $2,700 in total interest. Increasing monthly payments to $600 cuts the timeline to roughly 20 months and saves over $1,000 in interest.

Can I use the Snowball method if I have student loans?

Yes, student loans can be included in a Snowball sequence alongside credit cards and personal loans. Because federal student loans carry fixed rates and offer income-driven repayment options through the U.S. Department of Education, you may get more financial flexibility by keeping them on minimum payments and directing surplus funds to higher-rate revolving debt first.

Does paying off debt hurt your credit score?

Paying off installment loans (auto, personal) can cause a slight temporary score dip because it reduces credit mix diversity. Paying off revolving credit card balances almost always improves your FICO Score by reducing your utilization ratio. The net effect of a structured debt payoff plan is positive for most borrowers within 60 to 90 days.

What if I can only afford minimum payments right now?

Focus first on cutting expenses to free up even $50 to $100 per month. At the same time, contact your card issuers to request a hardship rate reduction, many will lower your APR temporarily if you ask directly. Even a small additional payment applied consistently to one target account outperforms scattered minimum payments across all accounts.

How do I pay off debt fast if my income is irregular?

Irregular income earners generally do better with the Snowball method, because each payoff milestone is achievable within a shorter payment window, reducing the risk of a missed month derailing a long campaign. Building a one-month cash buffer before starting aggressive payoff also insulates the plan from income gaps, a strategy covered in our guide on building a personal financial system.

Is debt consolidation better than Snowball or Avalanche?

Debt consolidation is a rate tool, not a sequencing strategy. It works best when you qualify for a loan rate meaningfully below your current blended APR. Once you consolidate, you still need a payoff method, Avalanche applied to a lower rate simply costs you less than either pure method would have at the original rates. Consolidation without a sequencing plan often leads to reborrowing on the cards you just paid off.

What is the biggest mistake people make when paying off debt?

Choosing a method and then abandoning it within the first three months. Most people quit during the early phase when balances have barely moved and motivation is lowest. Tracking interest saved rather than balance reduced, or deliberately starting with one small win, addresses that specific failure point better than any spreadsheet does.

Should I pay off debt or build an emergency fund first?

Build a small emergency buffer, $1,000 is a common starting target, before attacking debt aggressively. Without one, an unexpected expense forces you onto a credit card, which undoes recent progress and can break the repayment habit entirely. Once that buffer exists, direct full surplus payments to your chosen payoff method.